CIFC Asset Management’s Natalia Lojevsky and Stan Sokolowski provide their insights into the Fixed Income Markets, which have been experiencing an elevated bout of volatility as interest rates and inflation expectations have risen sharply. Stan and Natalia discuss the sea of red YTD for traditional fixed income returns and say we’re in a golden age for income producing alternatives.

In a “market mania,” retail investors are generally “long confidence” and “short experience” as the bubble inflates. While we often believe each “time” is different, it rarely is. It is only the outcomes that are inevitably the same.

The markets took a tumble to start last week as rising interest rates and inflationary pressures begin to weigh on outlooks. Those worries quickly diminished as Jerome Powell changed the rules to reassure Wall Street that “QE” is here to stay.

It can be difficult decide on a strategy and investment team in a sea of performance statistics. There is no perfect statistic or number for selecting a specific strategy; however, we believe some measures can be useful. This essay will walk through the common metrics used when discussing portfolio performance and provide some context for these numbers.

In a recent Nasdaq Markets publication, HANDLS Indexes Co-founder Matt Patterson provided a fourth quarter and year-end 2020 income investing recap. Matt also provided an outlook for 2021: well diversified portfolios with exposure to multiple asset classes continues to be the best protection against market dislocations.

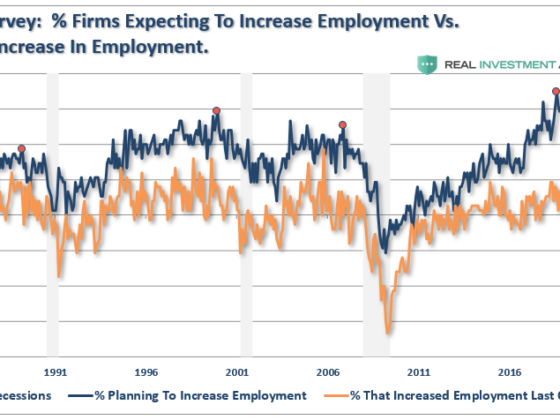

As discussed in Friday’s #Macroview, stimulus, mainly when it comes from debt, does not create organic economic growth. In the second part of this analysis, we delve into why Powell is wrong when he says more stimulus will solve the employment problem.

2021 has certainly started off interesting. From Reddit readers chasing the most heavily shorted stocks, to the new administration discussing more stimulus, investors have had plenty to deal with. A market review seems appropriate as the bulls seem to remain bulletproof even as the mania grows.

On an absolute basis, many markets and financial assets seem expensive relative to historic levels. However, as Barclays Capital notes, “Valuations may be detached from fundamentals but not reality.” Cash levels are enormous and numerous investors undoubtedly are sheltering in “safe” assets.

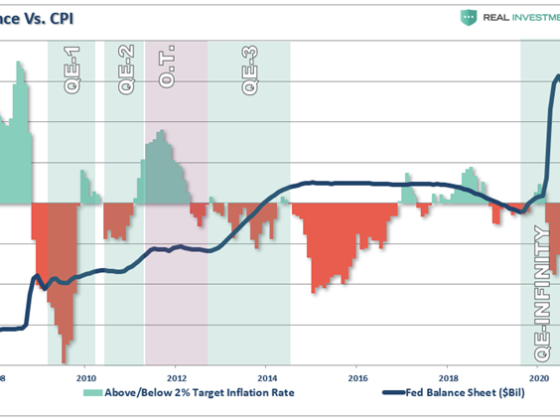

The Fed recognizes their ongoing monetary interventions have created financial risks in terms of asset bubbles. They are also aware that most policy tools are likely ineffective at mitigating financial risks in the future. Such leaves them being dependent on expanding their balance sheet as their primary weapon.