Dave Cohen is Cofounder of Bryant Avenue Ventures, an index provider which is implemented in a targeted distribution strategy at Strategy Shares. He previously served as Managing Director of Product Development at Guggenheim Investments. Dave is a product development executive with more than 20 years of experience creating successful financial products across a variety of asset classes and investment vehicles.

Investors seeking clarity on the future path of inflation and interest rates struggled to find it in March as key economic indictors sent mixed signals. The month kicked off with a strong February jobs report, with the Labor Department reporting that nonfarm payrolls increased by 275,000 for the month (against expectations of 198,000). While the February numbers suggested the economy continues to run hot, downward revisions to the December and January reports reduced the initial estimates for those months by 167,000 jobs and the unemployment rate rose from 3.7% to 3.9% in February.

Much like the Las Vegas Hotel on the Strip that appears to be right next door, investors are discovering in 2024 that interest rate cuts are farther away than they seem.

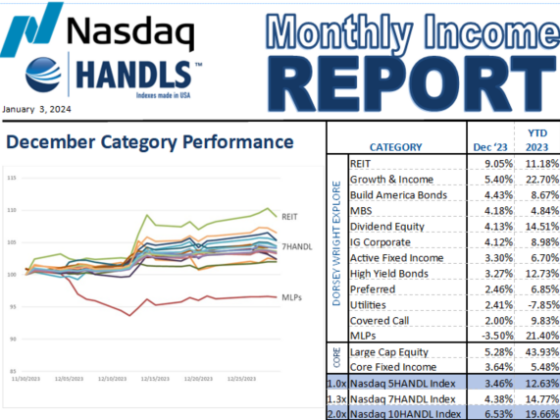

With the exception of MLPs, securities markets continued to deliver robust gains across the board in December as the markets began to divine measurable rate cuts by the Fed in 2024.

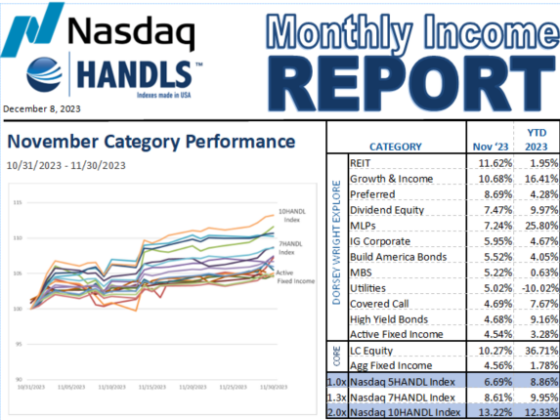

Securities markets shrugged off a challenging three months and delivered robust gains across the board in November as hopes for a soft economic landing gained ground among investors.

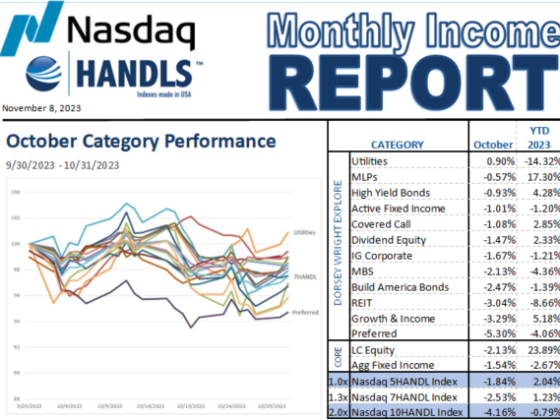

Securities markets continued to struggle in October in the face of rising interest rates and concerns about whether the Federal Reserve might continue its monetary tightening policy.

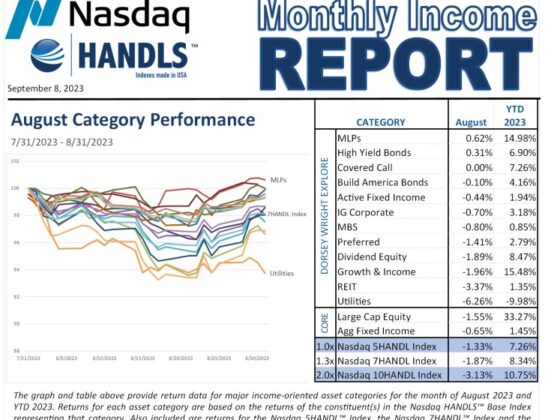

The Nasdaq 5HANDL Index was up 7.3% through the end of August, versus returns of 8.3% and 10.8% for the Nasdaq 7 HANDL Index and Nasdaq 10 HANDL Index, respectively.

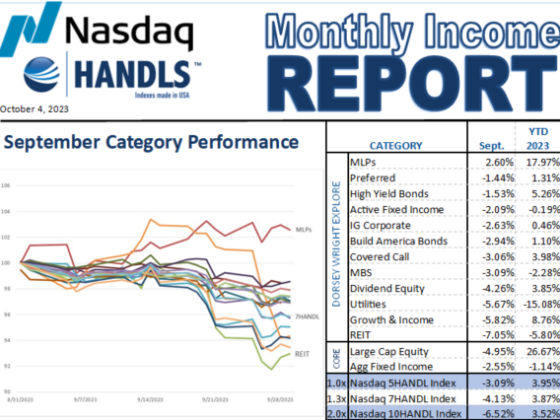

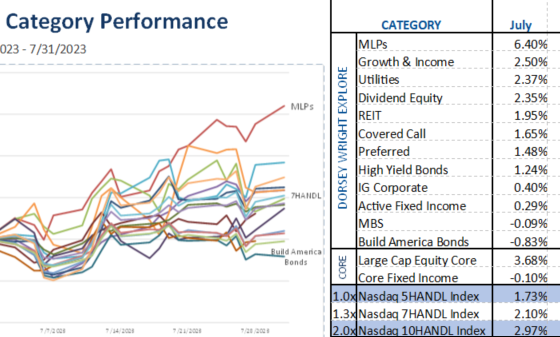

Equity categories that make up the Nasdaq Dorsey Wright Explore portion of HANDLS Indexes generally outperformed the fixed-income categories, with MLPs leading the way with a 6.4% return for the month.

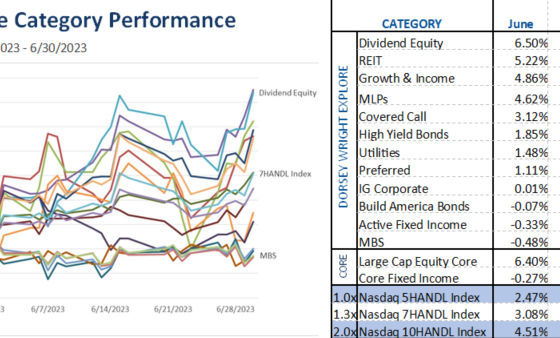

Markets were a mixed bag in June. Optimism about the Federal Reserve ending or at least slowing its rate-rising program pushed up the equity markets, with the Large Cap Core Equity category delivering a 6.4% return for the month. Nevertheless, inflation remained persistent, albeit at a lower annualized rate, and the Core Fixed Income category responded with a -0.3% return in June.