{kind=link}

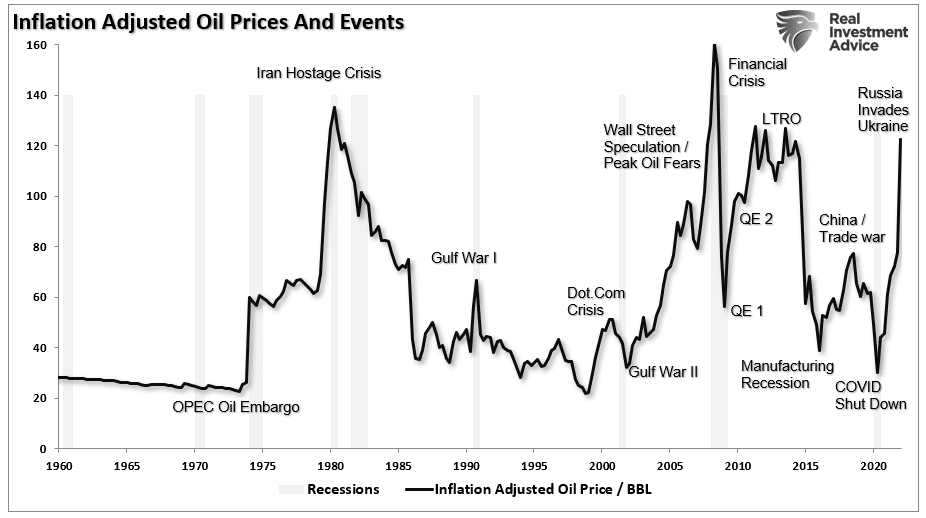

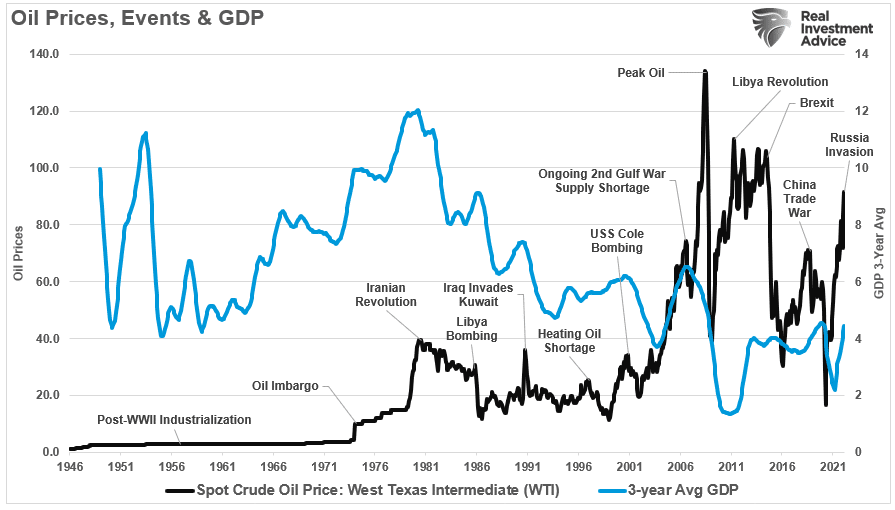

Oil spikes have historically negatively impacted economic outcomes. As the chart below shows, oil spikes typically are short-lived due to some exogenous geopolitical event. However, as was the case from 2003-2008, fundamental concerns, in this case, the fear of “peak oil,” can lead to more extended periods of higher prices.

The chart shows the inflation-adjusted price of oil since 1960.

While higher oil prices certainly benefit oil companies by making the extraction process more profitable, there is also a negative impact on the economy.

“High oil prices add to the costs of doing business. And these costs are area also ultimately passed on to customers and businesses. Whether it is higher cab fares, more expensive airline tickets, the cost of apples shipped from California, or new furniture shipped from China, high oil prices can result in higher prices for seemingly unrelated products and services.” – Investopedia

Of course, high oil prices are immediately noticeable by consumers who fill up their gas tanks each week. While economic reports of inflation strip out food and energy from the core calculation, the cost of food and fuel drives consumption patterns short term. Given that consumption comprises roughly 70% of the GDP calculation, the impact of higher oil prices is almost immediate.

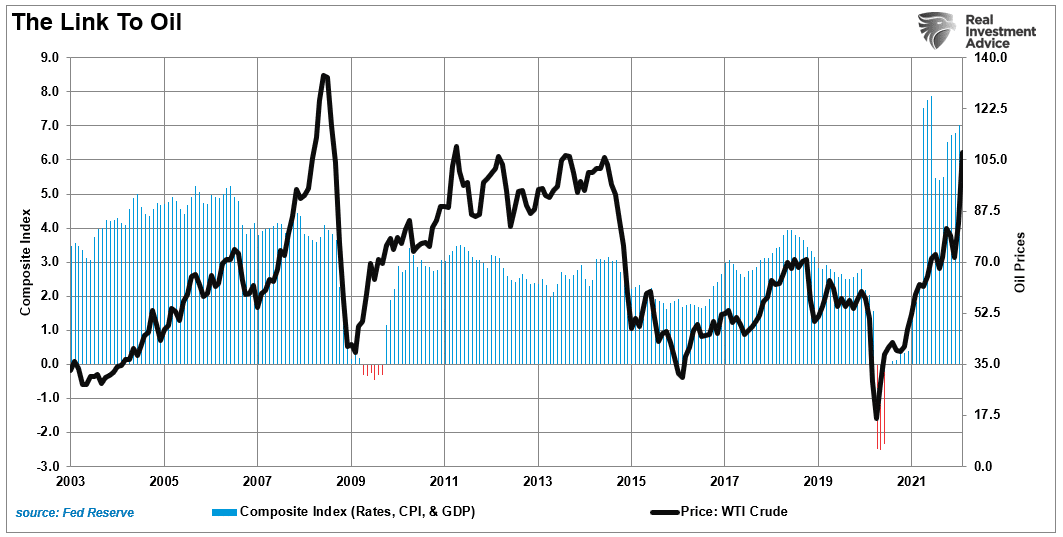

The Link To Oil

Oil prices are crucial to the overall economic equation. As such, there is a correlation between oil price, inflation, and interest rates.

We consume oil in virtually every aspect of our lives. From the food we eat to the products and services we buy. The demand side of the equation is a tell-tale sign of economic strength or weakness. We can see this clearly in the chart below, which combines rates, inflation, and GDP into one composite indicator.

Importantly, the oil industry is very manufacturing and production intensive. Therefore, price changes tend to be highly correlated to changes in the economic composite. While rising oil prices lead to an increase in manufacturing and CapEx, reducing consumption subtracts from economic growth.

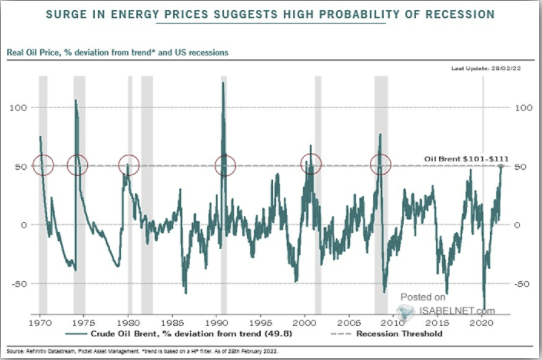

“It should not be surprising that sharp spikes in oil prices have been coincident with downturns in economic activity, a drop in inflation, and a subsequent decline in interest rates.“

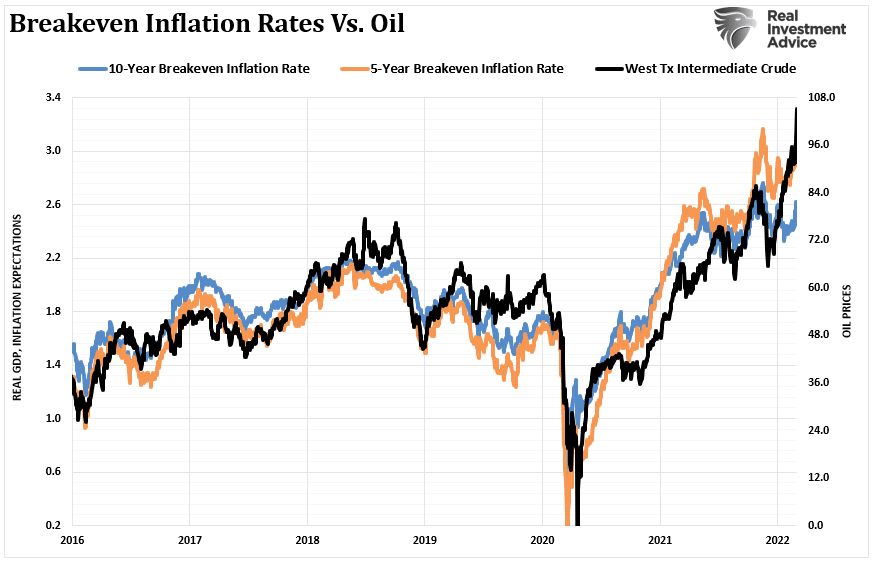

The most recent surge in oil prices started in early 2020. It was the direct result of the massive flood of fiscal policy, which created a consumption boom. However, this followed the collapse in oil prices as demand collapsed from the economic shutdown. Coincidentally, the surge in oil prices, and the pull-forward of consumption, led to surging inflationary pressures. We show the high correlation between oil prices and breakeven inflation rates.

The short version is that oil prices reflect supply and demand. Economic demand is weakening as liquidity reverses, and surging oil prices divert disposable incomes from other consumption needs.

As shown, the correlation between oil spikes and declines in economic growth (3-year average growth rate) should not be surprising.

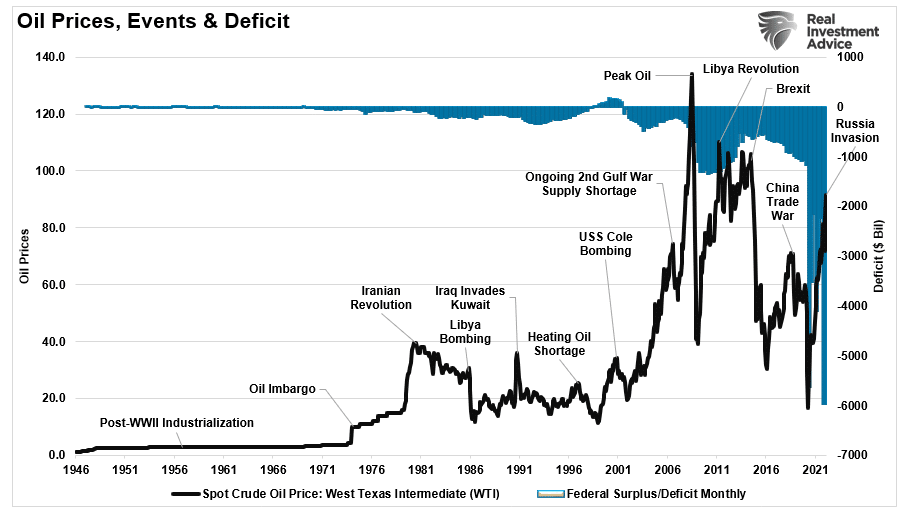

Oil Spikes And Deficit Spending

Not surprisingly, the flood of deficit spending in 2020 and 2021 led to a surge in inflationary pressures as well. As noted by Gail Tverberg in 2012, there is an unsurprising relationship.

“Increasingly high oil prices weaken an economy because they reduce discretionary spending and indirectly cause people to be laid-off from work. They have many other adverse effects as well–they tend to raise food prices, with similar effects. The laid-off workers require unemployment compensation payments, and at the same time, they are contributing less tax revenue. All of this creates a huge imbalance between revenue collected by governments and expenditures paid out. If oil prices rise again, it will tend to make the imbalance worse.

An economy such as the United States can cover up the problems caused by high oil prices with variety of financial techniques. In my view, high consumer confidence measures the success of those cover-ups, more than it measures the actual underlying situation. One way the US government manages to cover up how badly the economy is hurt by high oil prices is through deficit spending. Such remains continuous since late 2008, with outgoings exceeding income by more than 50% each year, even though the country is supposedly not in recession.

The amount consumers have available to spend on cars and gasoline is very much affected by deficit spending. With deficit spending, government employment can remain high and transfer payments can continue, without anyone really “paying” for these costs, putting more money into the economy to spend on oil and cars.”

Gail is correct. The problem is that since politicians see the “political goodwill” of “free money,” it is now their de facto “policy tool” for future recessions. As such, booms and busts will be continuously repeated in the future.

Will Oil Prices Cause A Recession, Depends On The Fed

The risk of a recession is rising. The surge in “artificial inflation” from the flood of liquidity against a supply shortage will eventually revert to a disinflationary trend. Debt and demographics will also continue to drive deflationary pressures leading to a reversal of the inflation trade.

However, for now, as the fear of inflation rose, investors piled into the commodity trade. While commodity prices rose due to the supply shortage, the reversal of that liquidity, and rebuilding of inventories, will ultimately undermine those assets. Such will coincide with a sharp decline in interest rates as deflation re-emerges.

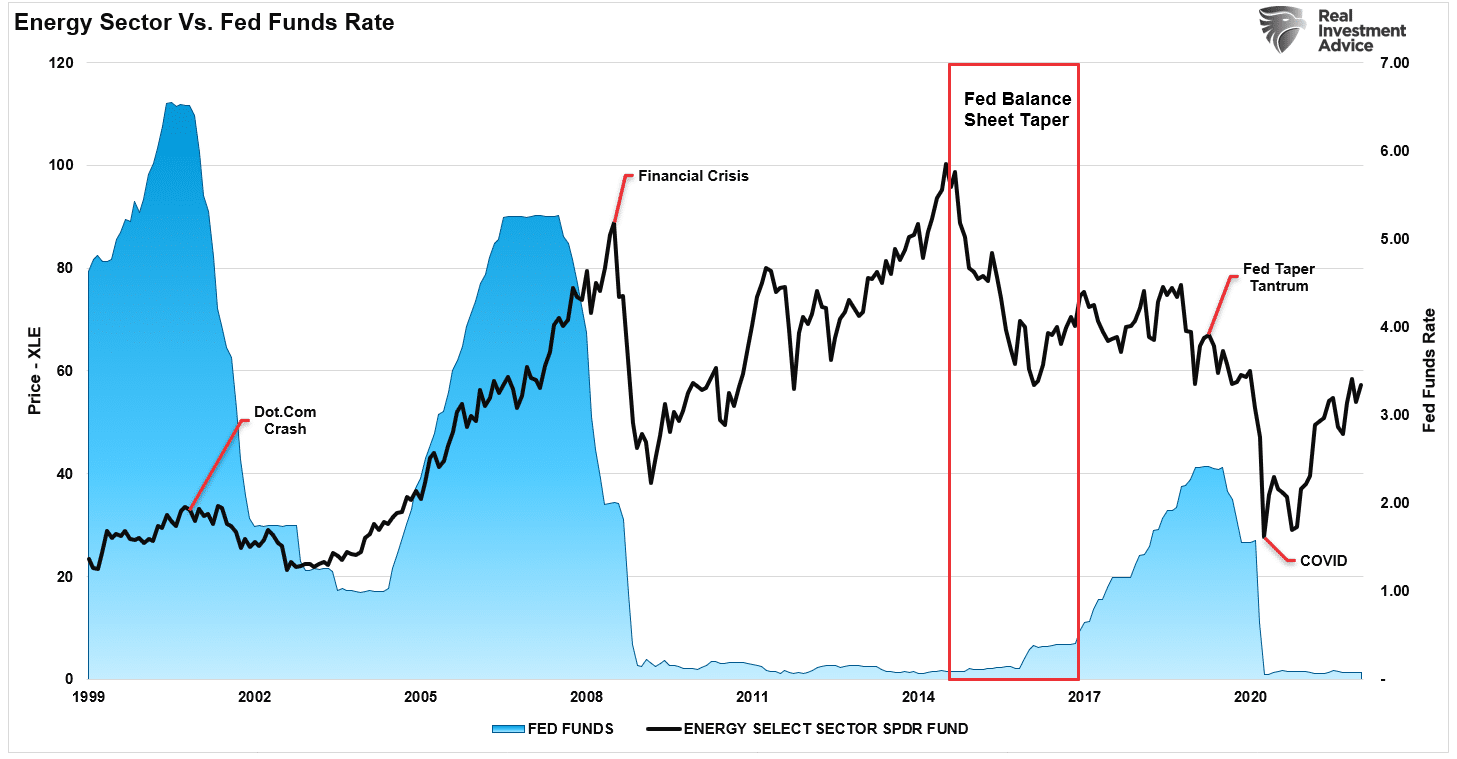

Of course, slowing economic growth and deflationary pressures will contribute to the decline in oil prices. One of the things that could generate that environment, sooner than later, is the Federal Reserve tightening its monetary policy.

Historically, when the Fed has hiked rates or tapered its balance sheet, oil prices fall due to slower economic growth. Such should not be surprising since oil prices are a function of supply and demand.

While the recent rally in energy stocks has been quite strong, the Fed is about to aggressively tighten monetary policy with the sole goal of combating inflation. In other words, to bring down inflation, they will slow economic growth, which reduces demand for commodity-based products.

Unfortunately, if history repeats, it won’t be just oil prices and energy stocks that get brought down in the process.