{kind=link}

Key Points

- The Fed “normalization” process is well under way. The damage has been severe.

- Attractive forward returns come from a willingness to buy quality stocks on sale.

- History shows buying industry leading brands after drawdowns tends to be wise.

The Fed’s “Normalization” Process Has Created Opportunities.

First, I hope you had a wonderful and relaxing holiday.

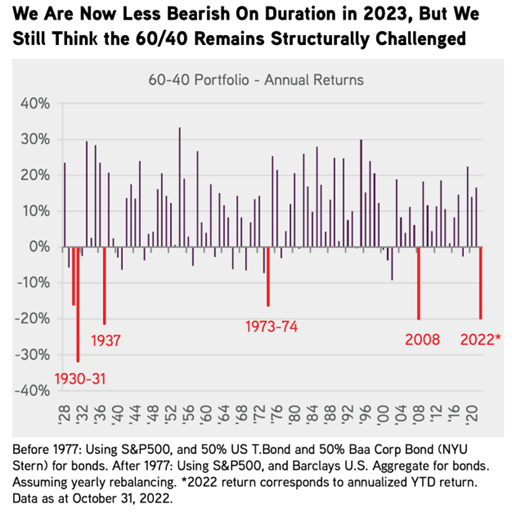

In case you missed last week’s blog, I’ll start with the same theme. There’s been significant damage to asset prices in 2022. Last year was one of the most difficult environments for investors in almost every asset class. Here’s the updated 60/40 portfolio yearly scorecard going back in time via a recent report from Private Equity leader, KKR:

We’ll start by covering the macro environment. In our opinion, it will be very hard to get back to a 2% inflation target, because frankly, 2% inflation was an anomaly. Between 1955 and 2006 when Ben Bernanke took over at the Fed, the average Fed Funds rate was just over 5% (we are headed back there), and the average inflation rate was about 4% (we see that as a more normal resting heart rate). This is “normal”, unlike 2% inflation and zero interest rates. Regardless, we are well on our way to normal but have a little more to go. As you know, the journey back to normal has been a rocky one. Asset prices have struggled mightily and now, some of the greatest companies ever created have seen 20-70% drawdowns for 2022. While painful to experience, drawdowns do allow savvy investors the opportunity to buy more of great businesses on sale. I think the concept of “buy low, sell high” is still a timeless approach to generating returns. I suspect you would agree.

The Old Adage: Buy Low, Sell High

Even average companies perform well in raging bull markets and strong economic cycles. It’s the more difficult periods when companies can set themselves apart from the peer group. Having the ability and interest to invest for the future while peers are retrenching is a hallmark of top companies (brands). Having a strong balance sheet to withstand difficult economic periods is vital. Generating significant free cash flow to make acquisitions, create new products, pay down debt, buyback stock, and pay dividends is also very important. We are now leaving the abnormal interest rate & inflationary environment we have been in since 2008. Zero interest rates and abnormally low inflation led to massive misallocations of capital and the creation of asset bubbles.

As the process of normalization continues, the road should be expected to stay rocky for a bit longer, but the opportunities created will be robust. As I write this commentary, sentiment towards equities continues to be extremely negative and general positioning in equities is underwhelming. The lack of committed buyers is what keeps a lid on any rallies for now but once we have some more clarity on the trajectory of rates & inflation, investors looking for bargains should get more attention. At some point in 2023, I suspect we will see a lot of buyers rushing through a narrow door as everyone tries to get “right-sized” in equities all at once. Today, it’s very difficult to find anyone bullish and very easy to find any number of dire bearish outcomes. That’s usually a decent time to start building more exposure to great businesses. Being a contrarian has always served me well, even if I was a bit early to the party.

Iconic Brands: A Long-Term History of Opportunity

Our team created the top global brands equity strategy because we understand that leading companies tend to outperform over long periods of time. Outperformance rarely happens every single year, that’s not realistic or required. The compounding effect of great businesses doing better than peers often leads to significant alpha generation. The trick: you must stay engaged during difficult times.

If you try to ride the best horses every year and jump to what you think will be the next greatest horse, you will invariably miss opportunities, create a tax headache, and feel like you are always chasing yesterday’s cheese. Peter Lynch’s success while running the Magellan Fund offers some great reminders to us all. When you have done the research and know your companies well, you get excited to buy more stock on sale. Mr. Lynch loved to average down when markets put his stocks on sale. The markets tend to be manic for periods of time but out of this manic behavior comes terrific buying opportunities. The best buying opportunities always happen in bear markets and when sentiment is poor. The bigger the opportunity, the more your stomach hurts when thinking about buying more. I remember adding to my favorite brands in February and March 2009, it felt horrible and made me a bit nauseous, but it was absolutely the right thing to do. That’s the way I feel going into 2023. It’s time to pick your spots and start planning your cost averaging strategy. If a company is still dominant in its category and the stock has suffered a deep drawdown, why would you not want to buy more? Maybe I’m crazy but I always feel like I’m cheating the system when the market gives me an opportunity to buy more shares of great businesses that are suffering short-term. When your time horizon is in the years, you should take these opportunities and put your hard-earned money to work at better prices. The history of markets has proven this over and over. If you follow my posts regularly, you’ll know how powerful cost averaging can be over time. As we get ready to enter 2023, we are being offered attractive entry points for our favorite companies. The best part, you don’t have to nail THE bottom, just committing to a cost average approach in tranches is all you need to do.

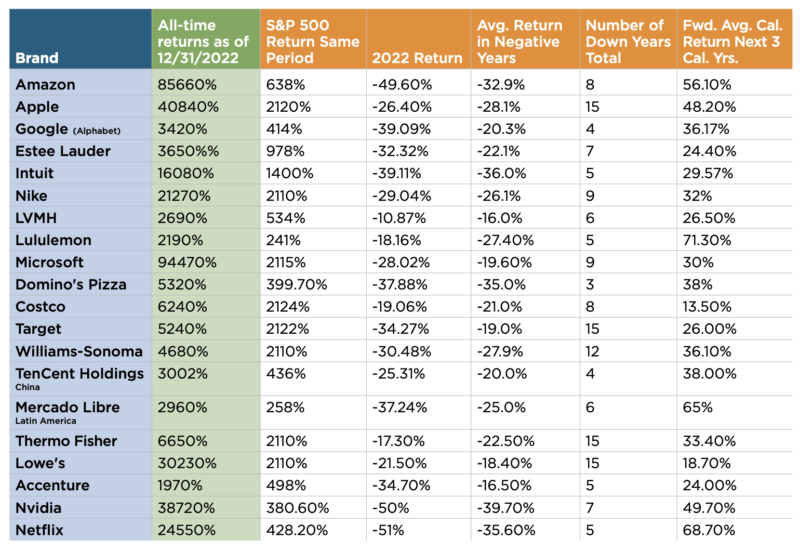

I thought it would be fun to take a handful of leading brands across different industries and show how they have performed since becoming public stocks. I compared them to the S&P 500 and then showed what the 2022 drawdown was, what the average drawdown in negative years was, and then looked back in history to see if buying those stocks after the negative year turned out to be a smart decision. Here’s the results. Shocker, buying great businesses after a big down year tended to offer a strong forward return experience. I expect the same result in the forward years. Again, there will always be demand for leading companies, particularly on mega sale so we all have a responsibility to take advantage of the market’s short-term spasms.

Included in this analysis: Amazon, Apple, Google, Estee Lauder, Intuit, Nike, LVMH, Lululemon, Microsoft, Domino’s Pizza, Costco, Target, Williams Sonoma, TenCent of China, Mercado Libre of Latin America, Thermo Fisher (life sciences tools), Lowes, Accenture, Nvidia, and Netflix. FYI, we own some of these brands at the current time and are looking at the others for opportunistic entries.

Data source: Morningstar, Ycharts & Accuvest.

The green column shows how each brand has performed since becoming a public company. These brands have performed incredibly well over the long term. The next column shows how the S&P 500 performed over the same period. The next vertical column shows how each brand performed in 2022. As we have learned already, there have been some extreme drawdowns this year. Most importantly, the last column shows the average of the 3 calendar years for each brand following a negative year. Great companies are not immune from deteriorating macro environments, but they do tend to take market share in tough times. As you can see from the long-term performance in the green column, even with multiple negative years, the long-term performance has been stellar.

No one knows what the future holds, maybe 2022 is just the beginning of a deeper down cycle for stocks but I feel confident that a willingness to own great businesses when the market acts irrationally and being willing to add to these stocks on sale, is ultimately a wonderful long-term opportunity for your portfolio. I add funds to my brands portfolio every single month and I feel confident my return on these investments will generate an attractive return because that’s the nature of investing in great businesses. Let’s be opportunistic in 2023!

Disclosure:

This information was produced by Accuvest and the opinions expressed are those of the author as of the date of writing and are subject to change. Any research is based on the author’s proprietary research and analysis of global markets and investing. The information and/or analysis presented have been compiled or arrived at from sources believed to be reliable, however the author does not make any representation as their accuracy or completeness and does not accept liability for any loss arising from the use hereof. Some internally generated information may be considered theoretical in nature and is subject to inherent limitations associated therein. There are no material changes to the conditions, objectives or investment strategies of the model portfolios for the period portrayed. Any sectors or allocations referenced may or may not be represented in portfolios managed by the author, and do not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that any investments in sectors and markets identified or described were or will be profitable. Investing entails risks, including possible loss of principal. The use of tools cannot guarantee performance. The charts depicted within this presentation are for illustrative purposes only and are not indicative of future performance. Past performance is no guarantee of future results.