{kind=link}

In a previous post “Market Bubbles,” I touched on George Soros’ “theory of reflexivity.” Interestingly, MarketWatch discussed with George why he no longer participates in the “bubble.” The foundation of his argument comes from his previous work in “Alchemy of Finance.” To wit:

“Pivoting to his legendary approach to financial markets, Soros acknowledges that investors are in a bubble fueled by Fed liquidity, which creates a situation that he now avoids. He explained that ‘two simple propositions’ make up the framework that has historically given him an advantage. However, since he shared it in his book, ‘Alchemy of Finance,’ the advantage is gone.” – MarketWatch

Specifically, he eludes to his “theory of reflexivity.”

“One is that in situations that have thinking participants, the participants’ view of the world is always incomplete and distorted. That is fallibility. The other is that these distorted views can influence the situation to which they relate, and distorted views lead to inappropriate actions. That is reflexivity.”

Before we get into the issue of “reflexivity,” let me recap what a “bubble” is.

Bubbles Are About Psychology, Not Metrics

“Market bubbles have NOTHING to do with valuations or fundamentals.”

Over the last few weeks, I have touched on the impact of valuations and forward returns. However, it is not just valuations, but also the surge in corporate debt and declining profitability resulting from weak economic growth. Historically, such a combination of factors is associated with previous “bear markets.”

None of these fundamental concerns are currently a problem. Despite the March selloff, 50-million unemployed, and a deep recession, the markets currently hover near all-time highs.

Such was a point George also confirmed:

“We are in a crisis, the worst crisis in my lifetime since the Second World War. I would describe it as a revolutionary moment when the range of possibilities is much greater than in normal times. What is inconceivable in normal times becomes not only possible but actually happens. People are disoriented and scared. They do things that are bad for them and for the world.”- George Soros

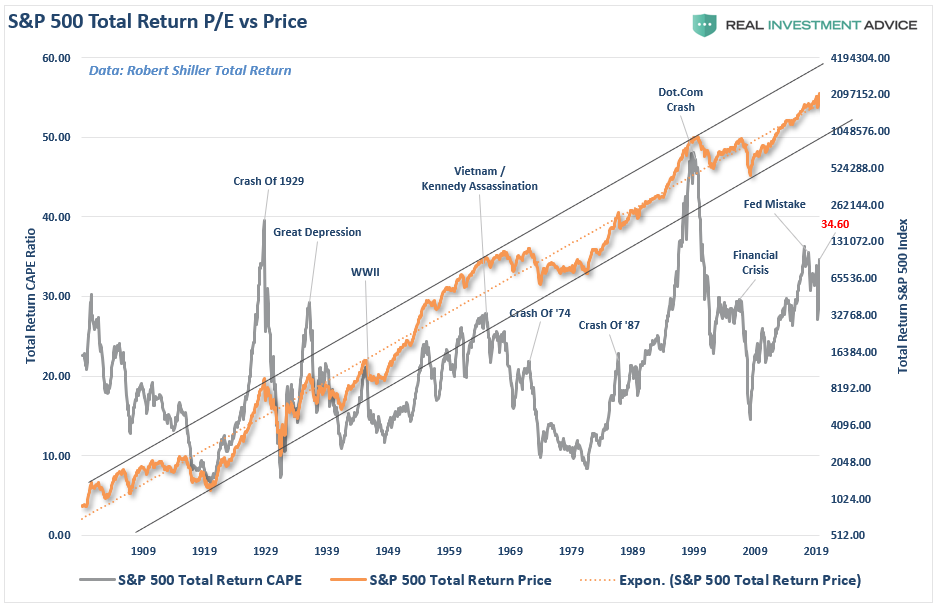

As shown in the chart below, the S&P 500 is trading in the upper 90% of its historical valuation levels.

However, since stock market “bubbles” reflect speculation, greed, emotional biases, valuations only reflect those emotions. As such, price becomes more reflective of psychology.

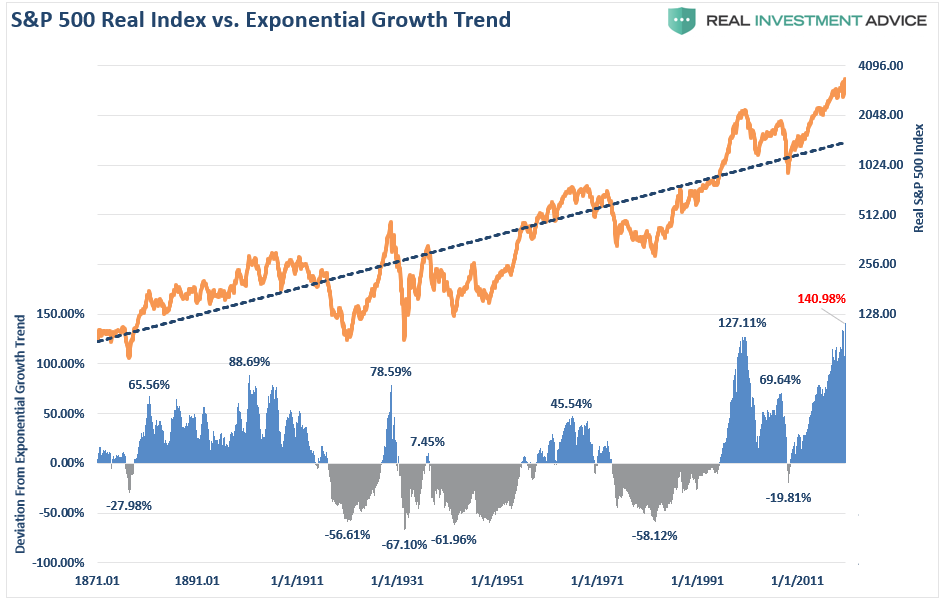

From a “price perspective,” the level of “greed” is on full display as the S&P 500 trades at the greatest deviation on record from its long-term exponential trend. (Such is hard to reconcile given a 35% correction just a few months ago.)

In other words, bubbles can exist even at times when valuations and fundamentals might argue otherwise. Notice that except for only 1929, 2000, and 2007, every other major market crash occurred with valuations at levels LOWER than they are currently.

A Basic Disregard

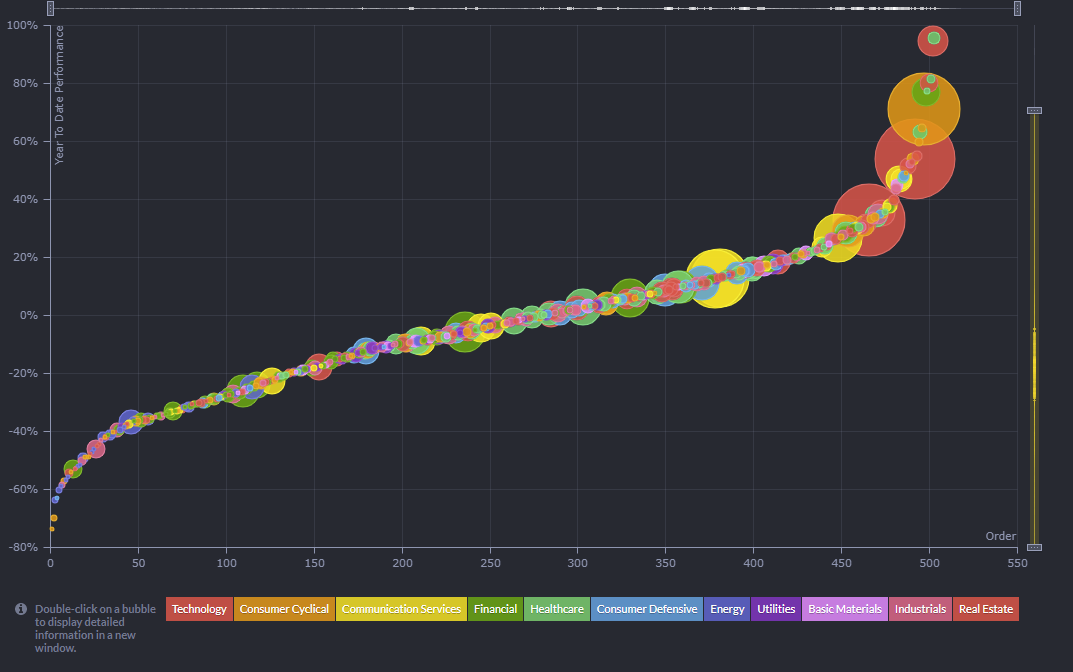

The chart, courtesy of Finviz.com, compares the year-to-date performance of the constituents of the S&P 500. The bigger the “bubble size,” the larger the market cap. Not surprisingly, the largest bubbles belong to the “mega-cap” stocks responsible for a majority of the market return. Importantly, notice the vast majority of stocks still sport negative returns.

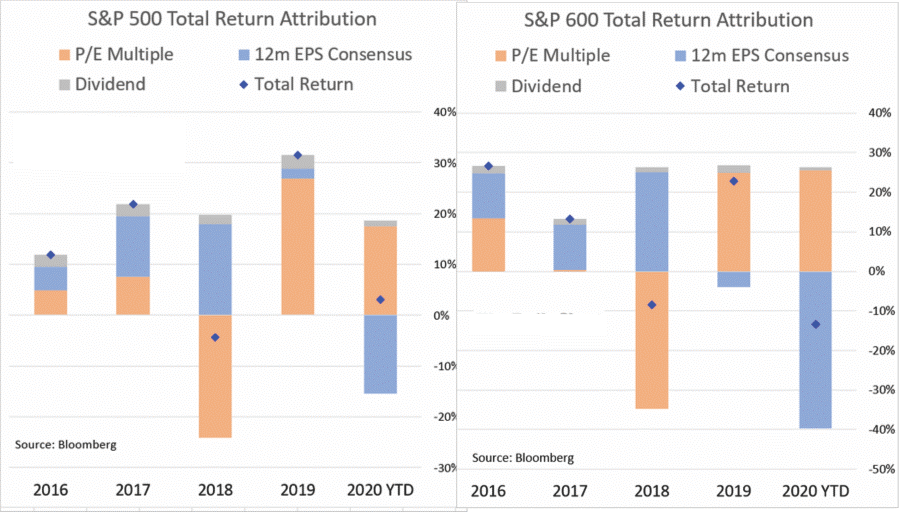

In other words, investors push valuations simply on “momentum.” As shown, since 2018, the increase in stock prices is primarily attributable to “valuation expansion.”

The basic disregard by investors over fundamental valuations is a reflection of the “psychological” bias now engulfing market participants. However, being excessively “bullish” is not what causes the eventual reversion. It is just the “fuel” that drives it.

No Bubble Is Ever the Same

Historically, all market crashes have been the result of things unrelated to valuation levels. Issues such as liquidity, government actions, monetary policy mistakes, recessions, or inflationary spikes are the culprits that trigger the “reversion in sentiment.”

Importantly, the “bubbles” and “busts” are never the same.

I previously quoted Bob Bronson on this point:

“It can be most reasonably assumed that markets are efficient enough that every bubble is significantly different than the previous one. A new bubble will always be different from the previous one(s). Such is since investors will only bid prices to extreme overvaluation levels if they are sure it is not repeating what led to the previous bubbles. Comparing the current extreme overvaluation to the dotcom is intellectually silly.

I would argue that when comparisons to previous bubbles become most popular, it’s a reliable timing marker of the top in a current bubble. As an analogy, no matter how thoroughly a fatal car crash is studied, there will still be other fatal car crashes. Such is true even if we avoid all previous accident-causing mistakes.”

Comparing the current market to any previous period in the market is rather pointless. The current market is not like 1995, 1999, or 2007? Valuations, economics, drivers, etc. are all different from cycle to the next.

Most importantly, however, the financial markets adapt to the cause of the previous “fatal crashes.” However, that adaptation won’t prevent the next one.

Alan Greenspan

Alan Greenspan, former chairman of the Federal Reserve, also noted the importance of investor behavior about both the buildup, and bust, of market bubbles. To wit:

“Thus, this vast increase in asset claims’ market value is partly the indirect result of investors accepting lower compensation for risk. Market participants too often view such an increase in market value as structural and permanent.

To some extent, those higher values may be reflecting the increased flexibility and resilience of our economy. But what they perceive as newly abundant liquidity can readily disappear. Any onset of increased investor caution elevates risk premiums and, as a consequence, lowers asset values and promotes the liquidation of the debt that supported higher asset prices. Such is why history has not dealt kindly with the aftermath of protracted periods of low-risk premiums.”

– Alan Greenspan, August 25th, 2005.

Credit Risk Is the Tell

Just as it was in 2005, we see much of the same behavior in the markets today. One of the “key arguments” for continuing to chase stocks has been that “low rates justifies taking on increased risk.” Such was a point Mr. Greenspan obviously disagreed.

“A decline in perceived risk is often self-reinforcing in that it encourages presumptions of prolonged stability and thus a willingness to reach over an ever-more extended period. But, because people are inherently risk-averse, risk premiums cannot decline indefinitely.

Whatever the reason for narrowing credit spreads, and they differ from episode to episode, history cautions that extended periods of low concern have invariably been followed by a reversal, with an attendant fall in the prices of risky assets. Such developments reflect not only market dynamics but also the all-too-evident alternating and infectious bouts of human euphoria and distress and the instability they engender.”

– Alan Greenspan, September 27th, 2005.

It’s not too hard to remember what happened next. In the short-term, investors always believe they can escape the eventual reversions of excess. In reality, they never do.

Soros’ Theory of Reflexivity

With this background, we can better understand Soros’ “theory of reflexivity.”

“Financial markets, far from accurately reflecting all the available knowledge, always provide a distorted view of reality. The degree of distortion may vary from time to time. Sometimes it’s quite insignificant, at other times, it is quite pronounced. When there is a significant divergence between market prices and the underlying reality, there is a lack of equilibrium conditions.

I have developed a rudimentary theory of bubbles along these lines.

Every bubble has two components: an underlying trend that prevails in reality and a misconception relating to that trend. When a positive feedback develops between the trend and the misconception, it sets a boom-bust process in motion. The process is liable to be tested by negative feedback along the way. If it is strong enough to survive these tests, it reinforces both the trend and the misconception.

Eventually, market expectations become so far removed from reality it forces people to recognize that a misconception is involved. A twilight period ensues during which doubts grow. More and more people lose faith, but the inertia sustains the prevailing trend.

As Chuck Prince, former head of Citigroup, said, ‘As long as the music is playing, you’ve got to get up and dance. We are still dancing.’ Eventually, the markets reach a tipping point and the trend reverses; it then becomes self-reinforcing in the opposite direction.

Typically bubbles have an asymmetric shape. The boom is long and slow to start. It accelerates gradually until it flattens out again during the twilight period. The bust is short and steep because it involves the forced liquidation of unsound positions.”

Asymmetry

The chart below is an example of asymmetric bubbles.

Soros’ view on the pattern of bubbles is interesting because it changes the argument from a fundamental view to a technical view. Prices reflect the psychology of the market, creating a feedback loop between the markets and fundamentals. As Soros stated:

“Financial markets do not play a purely passive role; they can also affect the so-called fundamentals they are supposed to reflect. These two functions that financial markets perform, work in opposite directions. In the passive or cognitive function, the fundamentals are supposed to determine market prices. In the active or manipulative function market, prices find ways of influencing the fundamentals. When both functions operate at the same time, they interfere with each other. The supposedly independent variable of one function is the dependent variable, so neither function has a truly independent variable. As a result, neither market prices nor the underlying reality is fully determined. Both suffer from an element of uncertainty that cannot be quantified.”

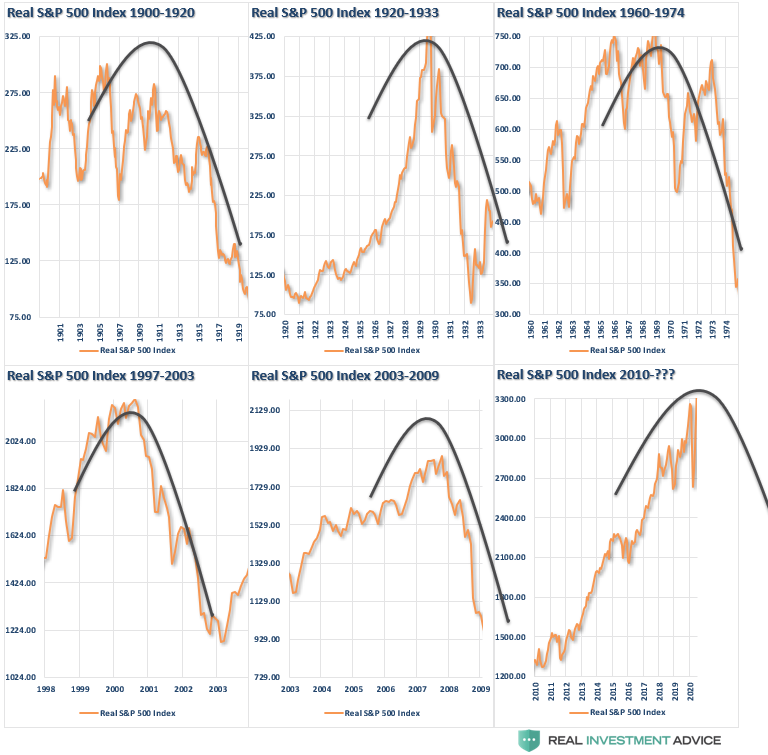

The chart below utilizes Dr. Robert Shiller’s stock market data going back to 1900 on an inflation-adjusted basis. I then took a look at the markets before each major market correction and overlaid Soros’ asymmetrical bubble shape.

Conclusion

There is currently much debate about the health of financial markets. Can prices remain detached from the fundamentals long enough for the economic/earnings recession to catch up with prices?

Maybe. It has just never happened.

The speculative appetite for “yield,” which has been fostered by the Fed’s ongoing interventions and suppressed interest rates, remains a powerful force in the short term. Furthermore, investors have now been successfully “trained” by the markets to “stay invested” for “fear of missing out.”

The increase in speculative risks, combined with excess leverage, leave the markets vulnerable to a sizable correction. The only missing ingredient for such a correction currently is simply the catalyst that starts the “panic for the exit.”

It is reminiscent of the market peak of 1929 when Dr. Irving Fisher uttered his now-famous words: “Stocks have now reached a permanently high plateau.”

Of course, that is most likely why Soros is choosing not to participate. At 90-years of age, these boom cycles are nothing new. However, he also knows how they end.

Do you?