{kind=link}

The Future Is Finally Here

After a year of waiting, investors were finally rewarded with an interest rate cut when the Federal Reserve’s Federal Open Market Committee (FOMC) cut the federal funds rate by 50 basis points (0.50%) on September 18th. In announcing the decision, the FOMC noted that it had “had gained greater confidence that inflation is moving sustainably toward 2 percent” and “that the risks to achieving its employment and inflation goals are roughly in balance.”

The FOMC’s decision followed August’s release of the Consumer Price Index (CPI) report. Monthly inflation came in at 0.2%, in line with expectations. For the 12-month period ending in August, inflation was 2.5%, the lowest level since February 2021. The Federal Reserve’s preferred inflation measure, the Personal Consumption Expenditures Index (PCE), offered even better news, with inflation coming in at 0.1% for August and 2.2% for the 12-month period.

Partly driving the FOMC’s decision were economic reports indicating a softening in what had been a robust economy. The Institute for Supply Management’s monthly survey of purchasing managers came in below expectations for August, while the Bureau of Labor Statistics jobs report indicated that nonfarm payrolls expanded by only 142,000 jobs during the month (against expectations of 161,000 jobs). Both the equity and bond markets responded favorably to the cut in interest rates, with the Core Large Cap Equity and Core Fixed categories gaining 2.5% and 1.3%, respectively, for the month of September.

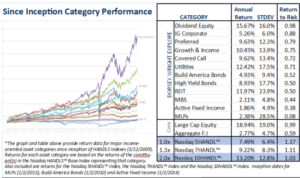

For the Nasdaq Dorsey Wright Explore portion of HANDLS Indexes, interest-rate-sensitive categories continued to be the biggest beneficiaries of softening inflation and lower interest rates. Utilities saw the biggest boost, gaining 6.6% for the month of September, pushing year-to-date returns to an eye-popping 30.2%. REITs also continued their recent hot strike, gaining 3.2% for the month. At the other end of the spectrum, MLPs were the worst performer for the third straight month (-0.4%) but remained up 17.8% on the year.

HANDLS indexes delivered positive returns across the board in September:

- Nasdaq 5HANDL™ Index: 1.8%

- Nasdaq 7HANDL™ Index: 2.2% (1.3x leveraged)

- Nasdaq 10HANDL™ Index: 3.2% (2.0x leveraged)

Disclosure: Nasdaq® is a registered trademark of Nasdaq, Inc. The information contained above is provided for informational and educational purposes only, and nothing contained herein should be construed as investment advice, either on behalf of a particular security or an overall investment strategy. Neither Nasdaq, Inc. nor any of its affiliates makes any recommendation to buy or sell any security or any representation about the financial condition of any company. Statements regarding Nasdaq-listed companies or Nasdaq proprietary indexes are not guarantees of future performance. Actual results may differ materially from those expressed or implied. Past performance is not indicative of future results. Investors should undertake their own due diligence and carefully evaluate companies before investing. ADVICE FROM A SECURITIES PROFESSIONAL IS STRONGLY ADVISED. © 2024. Nasdaq, Inc. All Rights Reserved

Important Disclosure. HANDLS Indexes receives compensation in connection with licensing its indices to third parties. Any returns or performance provided within are for illustrative purposes only and do not demonstrate actual performance. Past performance is not a guarantee of future investment results. It is not possible to invest directly in an index. Exposure to an asset class is available through investable instruments based on an index. HANDLS Indexes does not sponsor, endorse, sell, promote or manage any investment fund or other vehicle that is offered by third parties and that seeks to provide an investment return based on the returns of any index. There is no assurance that investment products based on an index will accurately track index performance or provide positive investment returns. HANDLS Indexes is not an investment advisor, and HANDLS Indexes makes no representation regarding the advisability of investing in any such investment fund or other vehicle. A decision to invest in any such investment fund or other vehicle should not be made in reliance on any of the statements set forth in this document. Prospective investors are advised to make an investment in any such fund or other vehicle only after carefully considering the risks associated with investing in such funds, as detailed in an offering memorandum or similar document that is prepared by or on behalf of the issuer of the investment fund or other vehicle. Inclusion of a security within an index is not a recommendation by Indexes to buy, sell, or hold such security, nor is it considered to be investment advice. The information contained herein is intended for personal use only and should not be relied upon as the basis for the execution of a security trade. Investors are advised to consult with their broker or other financial representative to verify pricing information for any securities referenced herein. Neither Indexes nor any of its direct or indirect third-party data suppliers or their affiliates shall have any liability for the accuracy or completeness of the information contained herein, nor for any lost profits, indirect, special or consequential damages. Either Indexes or its direct or indirect third-party data suppliers or their affiliates have exclusive proprietary rights in any information contained herein. The information contained herein may not be used for any unauthorized purpose or redistributed without prior written approval from HANDLS Indexes. Copyright © 2024 by HANDLS Indexes. All rights reserved.