{kind=link}

Does stock risk decline the longer the holding period is? It’s a great question and something I received a comment about.

Blaise Pascal, a brilliant 17th-century mathematician, famously argued that if God exists, belief would lead to infinite joy in heaven, while disbelief would lead to infinite damnation in hell. But, if God doesn’t exist, belief would have a finite cost, and disbelief would only have, at best a finite benefit.

Pascal concluded that given that we can never prove whether or not God exists, it’s probably wiser to assume he exists because infinite damnation is much worse than a finite cost.

When it comes to investing, Pascal’s argument applies as well. Let’s start with the following comment.

“The risk of buying and holding an index is only in the short-term. The longer you hold an index the less risky it becomes. Also, managing money is a fool’s errand anyway as 95% of money managers underperform their index from one year to the next.”

This is an interesting comment as it exposes two primary falsehoods.

Let’s start with the second comment, “95% of money managers can’t beat their index from one year to the next.”

The Great Con

One of the greatest cons ever perpetrated on the average investor by Wall Street is the “you can’t beat the index game.” It is true that many mutual funds underperform their index from one year to the next, but this has nothing to do with their long-term performance. The reasons that many funds and investors underperform in the short term are simple enough to understand if you think about what an index is versus a portfolio of invested capital.

- The index contains no cash

- It has no life expectancy requirements – but you do.

- It does not have to compensate for distributions to meet living requirements – but you do.

- It requires you to take on excess risk (potential for loss) to obtain equivalent performance – this is fine on the way up but not on the way down.

- It has no associated taxes, costs, or other expenses – but you do.

- It has the ability to substitute at no penalty – but you don’t.

- It benefits from share buybacks – but you don’t.

- It doesn’t have to deal with what “life” throws at it…but you do.

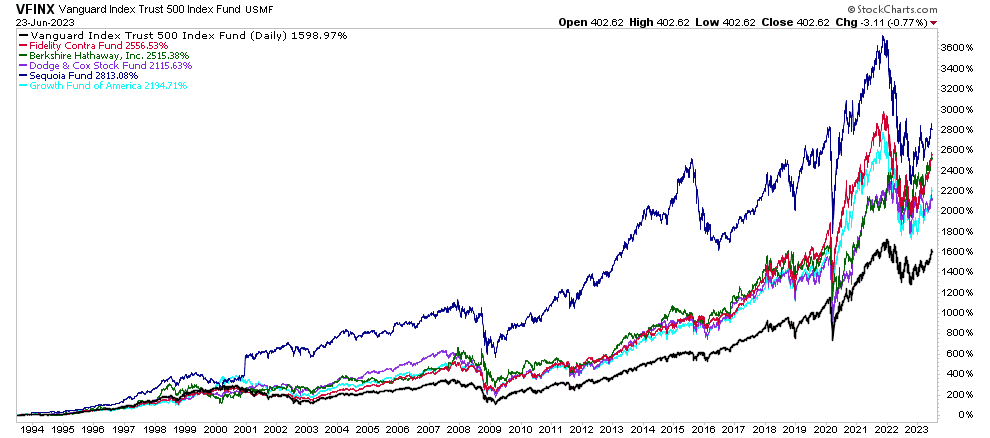

However, the myth of “active managers can’t beat their index” falls apart given time, as clearly shown in the chart below.

Oops. There are large numbers of active fund managers who have posted stellar returns over long-term time frames. No, they don’t beat their respective benchmarks every year, but beating some random benchmark index is not the goal of investing, to begin with. Investing aims to grow your “savings” over time to meet your future inflation-adjusted income needs without suffering large capital losses along the way.

Investing and avoiding major losses brings us to the first point of our comment that “stocks become less ‘risky’ over time.”

Stocks Become Less “Risky” Over Time?

This idea suggests the “stock risk” diminishes as time progresses.

First, the risk does not equal reward.

“Risk” is a function of how much money you lose when things don’t go as planned.

The problem with following Wall Street’s advice to be “all in – all the time” is that eventually, you will be dealt a bad hand. By being aggressive, and chasing market returns on the way up, the higher the market goes, the greater the risk that is being built into the portfolio. Most investors routinely take on more “risk” than they realize, exposing them to greater damage when markets undergo a reversion process.

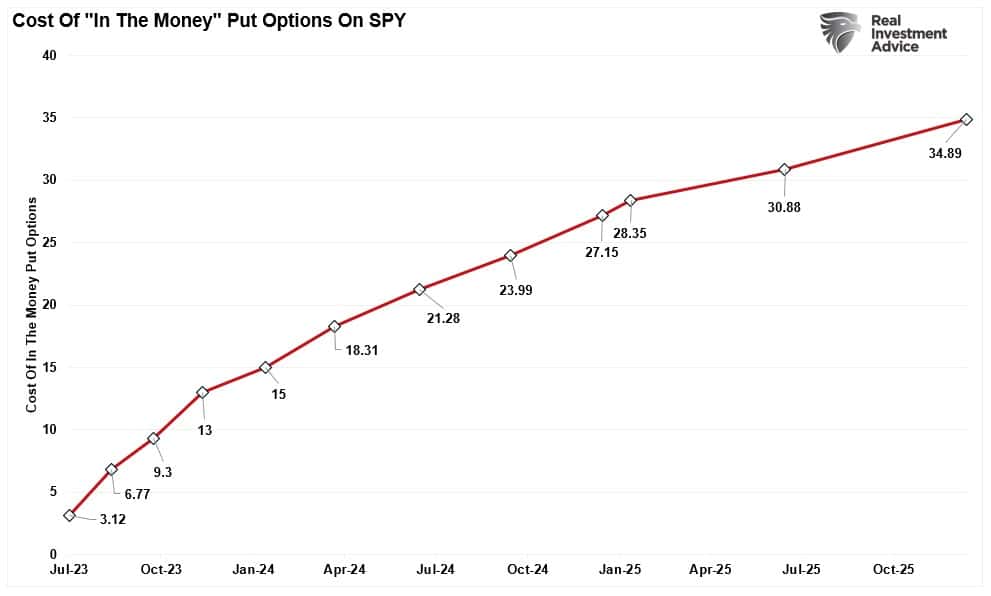

How do we know that stock risk increases over time? The cost of “insurance” tells us so. If the “risk” of ownership declines over time, then the cost of “insuring” the portfolio should also decline. The chart below shows the cost of buying insurance (put options) on the S&P 500 exchange-traded fund ($SPY).

As you can see, the longer a period our “insurance” covers, the more “costly” it becomes. This is because the risk of an unexpected event that creates a loss in value rises the longer an event doesn’t occur.

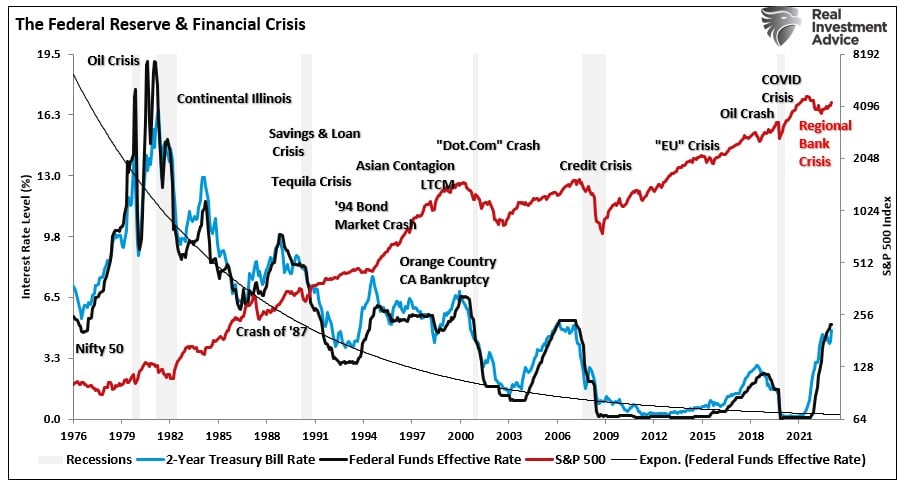

Furthermore, history shows that large drawdowns occur with regularity over time. Such is particularly true when the Federal Reserve tightens monetary policy by hiking rates.

Yes, the financial markets over the last decade, due to massive monetary accommodation, defied the laws of fundamentals and logic.

But as Mr. Pascal suggests, even if the odds of something happening are small, we should still pay attention to that slim possibility if the consequences are dire. Rolling the investment dice while saving money by skimping on insurance may give us a shot at amassing more wealth, but with that chance of greater success comes a risk of devastating failure.

Winning The Long Game

In golf, there is a saying that you “drive for show and putt for dough,” meaning that it is not necessary to be able to drive a golf ball 300 yards down the center of the fairway. The skill of putting, measured in feet, will win the game.

Investing is much the same. Investing in the market is one thing. However, understanding the “short game” of investing is critically important to winning the “long game.”

When valuations rise to rarely seen levels, and the associated risks of a major drawdown increase exponentially, investor should focus on managing the “stock risk” of the portfolio rather than chasing “returns.”

Investors would do well to remember the words of the then-chairman of the Securities and Exchange Commission, Arthur Levitt, in a 1998 speech entitled “The Numbers Game:”

“While the temptations are great, and the pressures strong, illusions in numbers are only that—ephemeral, and ultimately self-destructive.”

But it was Howard Marks who summed up our philosophy on “risk management” well when he stated:

“If you refuse to fall into line in carefree markets like today’s, it’s likely that, for a while, you’ll (a) lag in terms of return and (b) look like an old fogey. But neither of those is much of a price to pay if it means keeping your head (and capital) when others eventually lose theirs. In my experience, times of laxness have always been followed eventually by corrections in which penalties are imposed. It may not happen this time, but I’ll take that risk.”

Clients should not pay a fee to mimic markets. Fees should be paid to investment professionals to employ an investment discipline, trading rules, portfolio hedges, and management practices proven to reduce the probability of serious and irreparable impairment to their hard-earned savings.

Unfortunately, the rules are REALLY hard to follow. If they were easy, then everyone would be wealthy from investing. They aren’t because investing without discipline and strategy has horrid consequences.

Personally, I choose to “believe” as I really don’t like the sound of “eternal damnation.”

The post Stock Risk – Does It Decline Over Time? appeared first on RIA.