{kind=link}

Bullish investors continue to “Fight the Fed,” hoping that a change to monetary policy will reignite the 12-year-long bull market. But, for over a decade, the “Don’t Fight The Fed” mantra was the “call to arms” for bullish investors.

“With zero interest rate policies and the most aggressive monetary campaign in history, investors elevated the financial markets to heights rarely seen in human history. Yet, despite record valuations, pandemics, warnings, and inflationary pressures, the “animal spirits” fostered by an undeniable “faith in the Federal Reserve.”

Of course, the rise in “animal spirits” is simply the reflection of the rising delusion of investors who frantically cling to data points that somehow support the notion ‘this time is different.’”

Not surprisingly, as a massive flood of monetary interventions detached market dynamics from economic and fundamental realities, bullish investors scrambled to find rationalizations for ever-higher asset prices. David Einhorn previously explained such:

“The bulls explain that traditional valuation metrics no longer apply to certain stocks. The longs are confident that everyone else who holds these stocks understands the dynamic and won’t sell either. With holders reluctant to sell, the stocks can only go up – seemingly to infinity and beyond. We have seen this before.

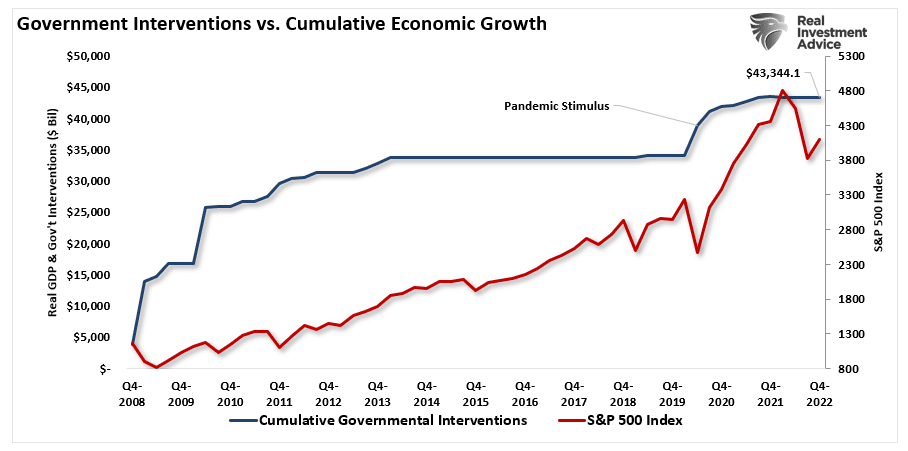

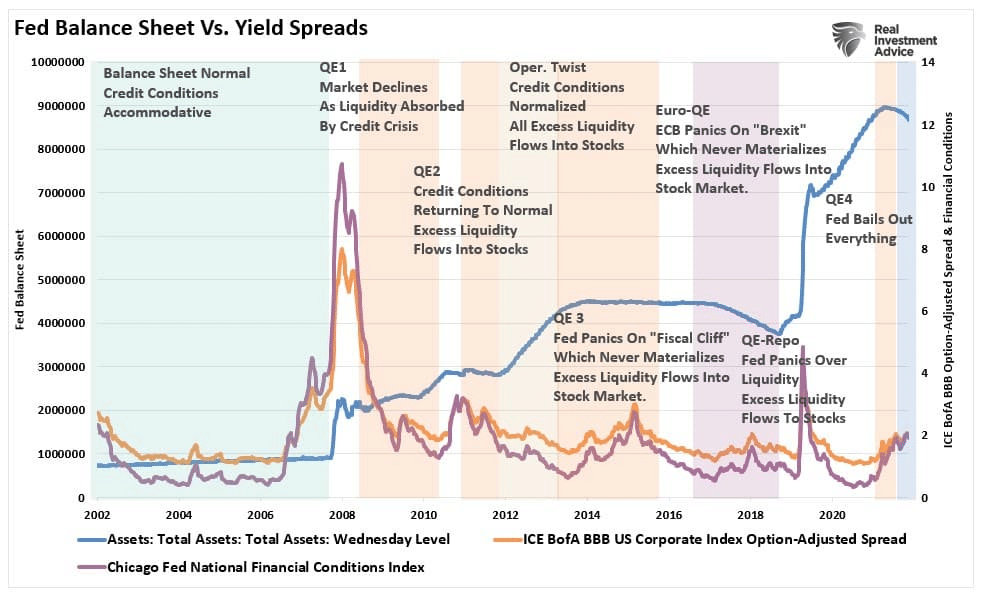

Of course, with more than $43 Trillion in bailouts and Federal Reserve interventions, it is of no surprise that bullish investors cast caution to the wind.

It is also not surprising that stocks have come under pressure as the Fed started hiking interest rates aggressively and the process of reducing its previous influx of monetary support.

Yet, instead of bullish investors sticking with their mantra of “Don’t Fight The Fed,” it is now a standoff between bullish investors and the Fed. After a tough year in the markets, the hope for 2023 is that the Fed will “pivot” in its monetary policy campaign and begin to ease by mid-year. As Tom Lee of FundStrat noted;

“Historical data shows there is a high chance that the U.S. stock market may record a return of 20% or more this year after the three major indexes closed 2022 with their worst annual losses since 2008,”

While bullish investors cling to historical statistics about market returns, the problem is the Fed remains clear that it will not back off its current inflation fight.

The Fed And Bullish Investors Are At Odds

In early January, the market got the release of the minutes from the December FOMC meeting. The minutes were unsurprising, at least to us, as they reiterated the same message the FOMC delivered in all of 2022. To wit:

“No participants anticipated that it would be appropriate to begin reducing the federal funds rate target in 2023. Participants generally observed that a restrictive policy stance would need to be maintained until the incoming data provided confidence that inflation was on a sustained downward path to 2 percent, which was likely to take some time. In view of the persistent and unacceptably high level of inflation, several participants commented that historical experience cautioned against prematurely loosening monetary policy.”

There are a couple of important points made in that statement.

- The FOMC isn’t looking to have inflation at 2% before changing its policy stance. They want to see a clear and sustained pathway to 2%.

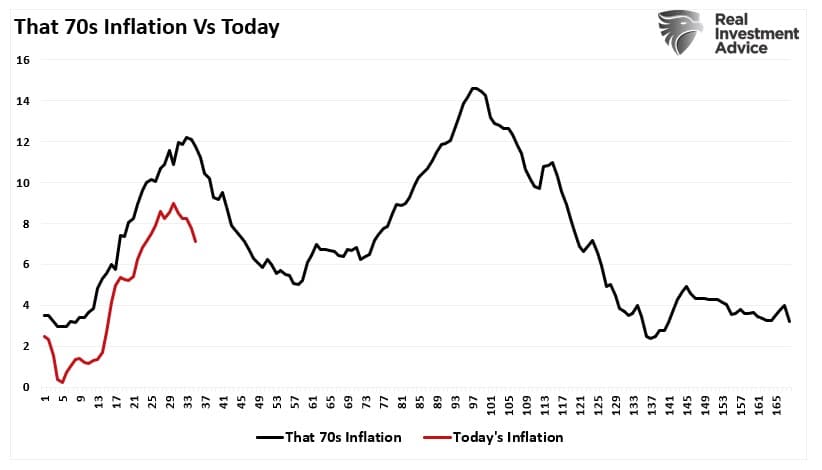

- The FOMC fears inflation will come down and then reaccelerate, as seen in the 70s. (See chart)

It is worth noting that the floor for inflation in the 70s was 4% versus 2% today. Such is because debt levels were dramatically lower, economic growth was more robust, and there was no Federal deficit. Today, the economy can’t sustain higher interest rates or inflation for very long without more severe economic consequences.

Nonetheless, despite the FOMC reiterating there is “no pivot” coming on monetary policy anytime soon, bullish investors expect rate cuts as soon as July of this year.

Notably, bullish investors are trying to apply some fundamental logic for a stronger market in 2023.

- The economy will avoid a recession.

- Employment will remain strong, and wages will see the consumer through.

- Corporate profit margins will remain elevated, thereby supporting higher market valuations.

- The Fed will back off its tightening campaign as inflation falls.

There is a particular problem with those arguments.

If the economy and employment remain strong, and a recession gets avoided, there is no reason for the Fed to begin cutting rates. Yes, the Fed may stop hiking rates, but if the economy is functioning normally and inflation is falling, there is no reason for rate cuts.

More importantly, bullish investors continue to work against their own interests.

The Beatings Will Continue Until Morale Improves

As we discussed, the Fed wants “tighter,” not “looser,” financial conditions.

“Higher asset prices represent looser, not tighter, monetary policy. Rising asset prices boost consumer confidence and act to ease the very financial conditions the Fed is trying to tighten. While financial conditions have tightened recently between higher interest rates and surging inflation, they remain low. Such is hardly the environment desired by the Fed to quell inflation.”

The FOMC needs substantially tighter financial conditions to slow economic demand and increase unemployment, lowering inflation toward target levels. Tighter financial conditions are a function of several items:

- A stronger US dollar relative to other currencies (Check)

- Wider spreads across bond markets (There is no credit stress currently)

- Reduction in liquidity (Quantitative Tightening or QT)

- Lower stock prices.

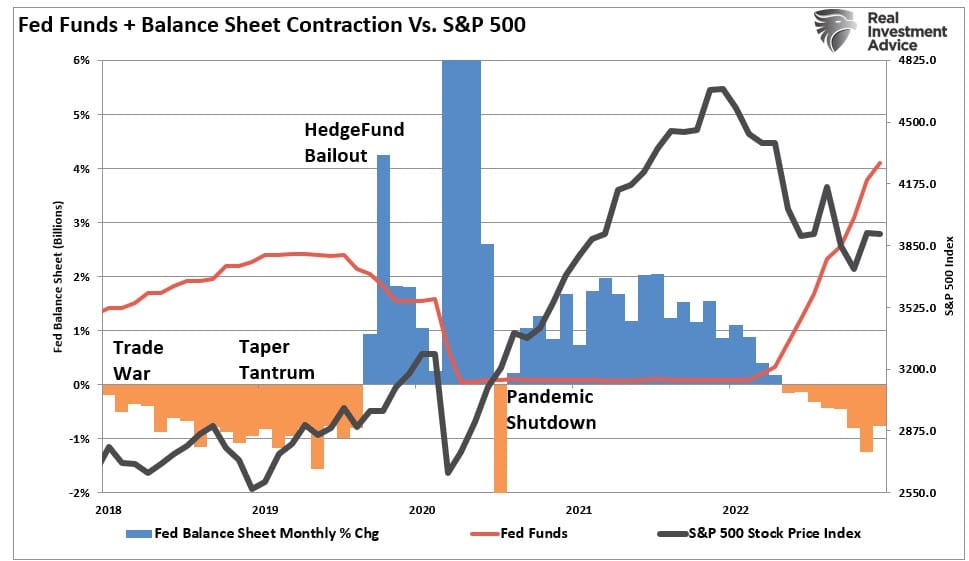

The more bullish market participants should be aware the Fed is ultimately pushing for lower stock prices. The Fed is removing liquidity by reducing its balance sheet twice as fast as in 2018. For those who don’t remember, the last QT ended in a 20% market plunge over three months. Today, even with weaker inflation, QT is not ending anytime soon.

We noted in November that:

It will not be surprising to see Federal Reserve speakers try and swat down asset prices with continued hawkish rhetoric. As far as a ‘pivot’ goes, that still seems quite a long way off.”

That point was repeated in the latest FOMC minutes.

“Participants noted that, because monetary policy worked importantly through financial markets, an unwarranted easing in financial conditions, especially if driven by a misperception by the public of the Committee’s reaction function, would complicate the Committee’s effort to restore price stability. Several participants commented that the medians of participants’ assessments for the appropriate path of the federal funds rate in the Summary of Economic Projections, which tracked notably above market-based measures of policy rate expectations, underscored the Committee’s strong commitment to returning inflation to its 2 percent goal.”

As noted, the FOMC wants a “controlled burn” of asset prices lower, not higher. I would suspect that at some point, market participants will realize that the FOMC is serious about its mission.

However, for now, hope remains.

Risks Of A Recession Are Elevated

As noted, heading into 2023, market participants are starting to coalesce around the idea the economy will avoid a recession. To wit:

“We believe the Fed will stop QT sometime in the Fall before they begin lowering rates. It is hard for us to see a recession of any significance occurring in 2023.” – Brett Ewing, Chief Market Strategist, First Franklin.

Maybe that happens. Anything is certainly a possibility.

However, that is essentially swimming against the stream of what the FOMC is trying to achieve. Again, if the goal is to quell inflation, then economic demand must fall. Even the FOMC is now admitting a recession is plausible.

“Moreover, the sluggish growth in real private domestic spending expected over the next year, a subdued global economic outlook, and persistently tight financial conditions were seen as tilting the risks to the downside around the baseline projection for real economic activity, and the staff still viewed the possibility of a recession sometime over the next year as a plausible alternative to the baseline”

The financial markets have yet to adjust to accommodate for a substantially weaker, if not recessionary, economy.

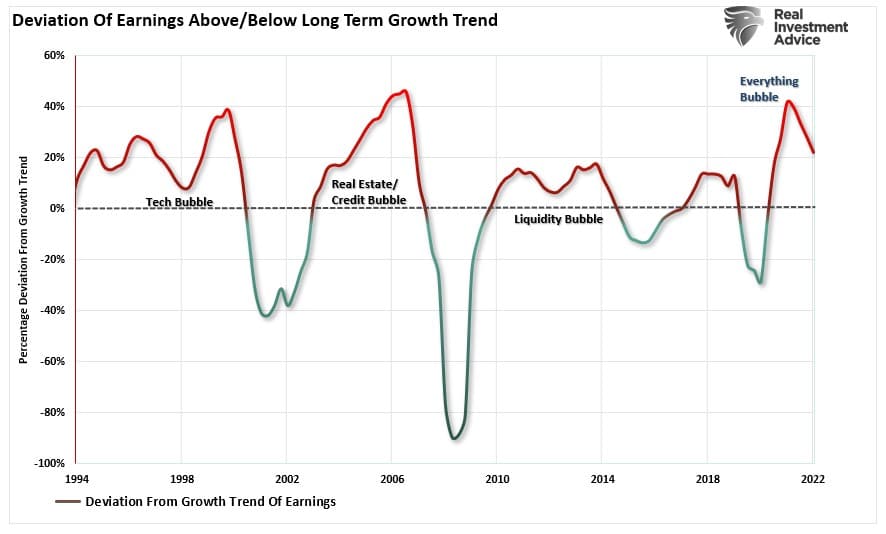

As discussed previously, earnings estimates remain highly optimistic and deviated from their long-term growth trend despite the recent cuts.

As my friend and colleague Albert Edwards of Societe Generale recently noted:

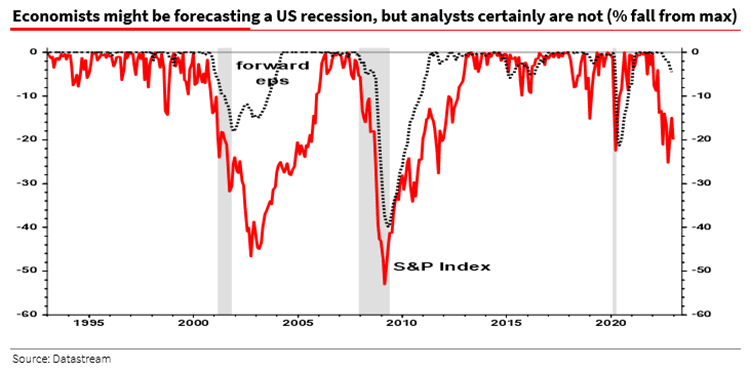

“I keep being told this is the most widely anticipated recession ever, and it must already be priced in. But the decline in 12-month forward EPS of only 4% (from the peak) doesn’t suggest so.”

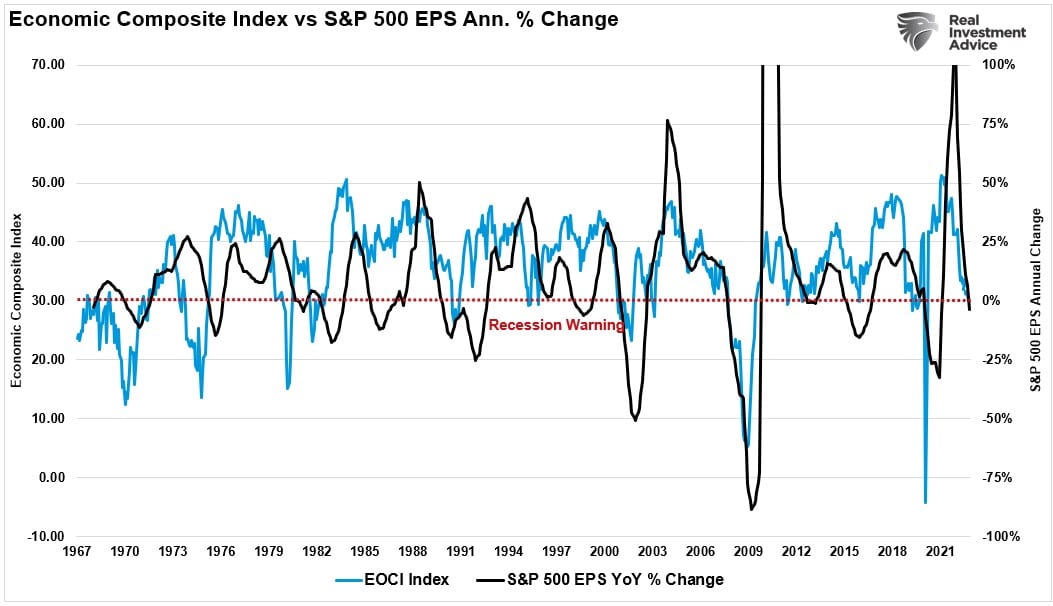

Furthermore, the rash of weak economic data also suggests that the risk of a recession has risen markedly, as noted by our broad economic activity composite index. If that data weakens further, which is the Fed’s goal, such also suggests lower earnings.

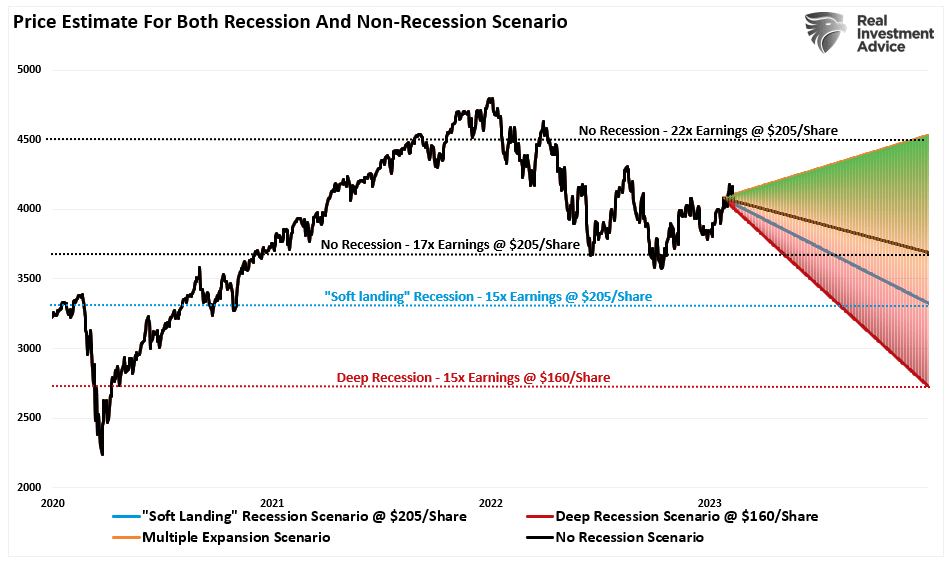

Given current valuations, as discussed in more detail here, the forecast for asset prices later in the year is not extremely bullish.

“Adding the bullish scenario to our projection chart gives us a full range of options for 2023, which run the gamut from 4500 to 2700, depending on the various outcomes.”

Here is our concern with the bullish scenario. It entirely depends on a “no recession” outcome, and the Fed must reverse its monetary tightening. The issue with that view is that IF the economy does indeed have a soft landing, there is no reason for the Federal Reserve to reverse reducing its balance sheet or lower interest rates.

More importantly, the problem with the bullish forecast is the rise in asset prices eases financial conditions, which reduces the Fed’s ability to bring down inflation. Such would also presumably mean employment remains strong along with wage growth, elevating inflationary pressures.

While the bullish scenario is possible, that outcome faces many challenges in 2023, given the market already trades at fairly lofty valuations. Even in a “soft landing” environment, earnings should weaken, which makes current valuations at 22x earnings more challenging to sustain.

While bullish investors continue trying to “Fight the Fed,” such may prove to be a more formidable challenge than many expect.

The post Bullish Investors Continue To Fight The Fed appeared first on RIA.