{kind=link}

As expected, Wall Street wins again. In 2020 and 2021, retail investors were chasing financial markets recklessly. Armed with sites like Reddit WallStreetBets and a Robinhood trading app, not to mention young investing mentors on social media, they believed they had the Wall Street “tiger by the tail.”

In January, we warned investors (mostly falling on deaf ears) that 2022 would likely be disappointing. To wit:

“From the mainstream media’s view, expectations are high that 2022 will be a continuation of 2021. Maybe such will be the case. However, as we laid out just recently, many of the headwinds that supported the ramp in speculative behaviors have, or will, reverse in the months ahead.”

- Tighter monetary policy and high valuations.

- Less liquidity globally as Central Banks slow accommodation.

- Less liquidity in the economy as the previous financial injections fade.

- Higher inflation reduces consumption.

- Weaker economic growth

- Weak consumer confidence due to inflation

- Flattening yield curve

- Weaker earnings growth

- Profit margin compression

- Weaker year-over-year comparisons of most economic data.

“As is always the case, the event that changes the “bullish psychology” is always unknown. However, the eventual market reversion is almost always a function of changes in liquidity or a contraction in earnings.

Most notably was the concluding sentence.

“Heading into 2022, a review of 2021 can undoubtedly provide some clues as to what potentially happens next. Notably, “record levels” of anything are records for a reason as it denotes the last period before the eventual reversion.“

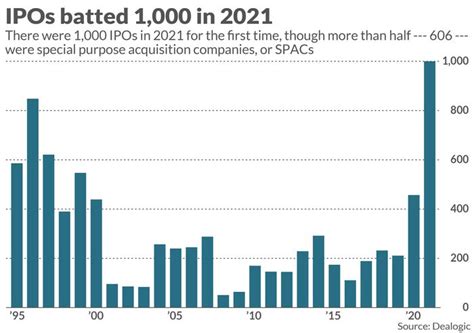

In 2020 and 2021, we saw record IPO and SPAC issuance levels. Wall Street was happy to feed the stimulus-check-fueled feeding frenzy of retail investors.

Everyone forgot to ask, “why am I so lucky to get access to this investment?”

Wall Street Wins Again

It was interesting to hear retail investors crowing in chat rooms about how they were beating Wall Street at their own game. Such is not surprising given the massive gains retail traders made by taking on an excessive amount of risk and doing so with leverage.

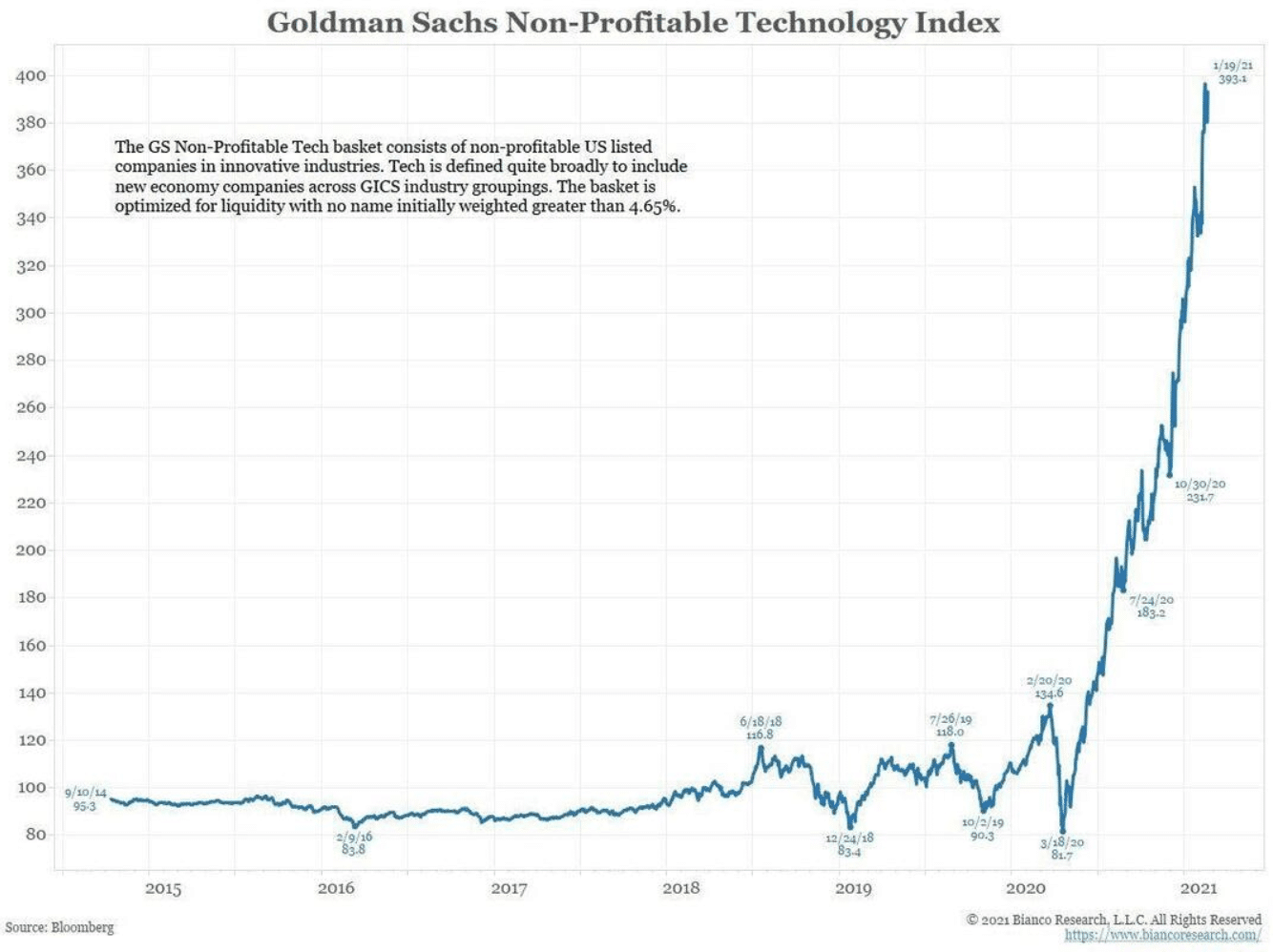

As shown below, investors were eager to buy the IPOs of companies even though most of them generated no profits.

Special purpose acquisition vehicles (SPACs) were relatively unused until the firehose of pandemic liquidity spurred Wall Street capital markets teams into action, forming hundreds of companies to raise billions of dollars of equity in these so-called blank-check offerings.

However, as noted, retail traders forgot to ask WHY Wall Street offered this incredible opportunity to invest in these start-up companies? After all, if these companies are so valuable, why wouldn’t Wall Street keep these prized possessions?

But in a “speculative market,” such is not surprising. What is not surprising is how it ended.

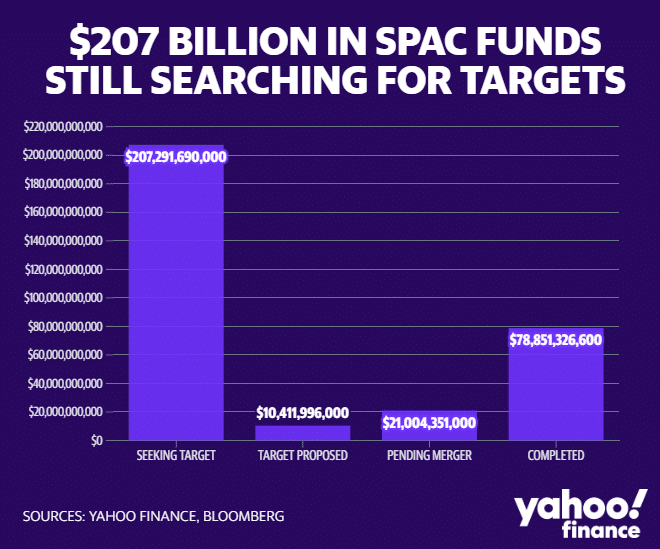

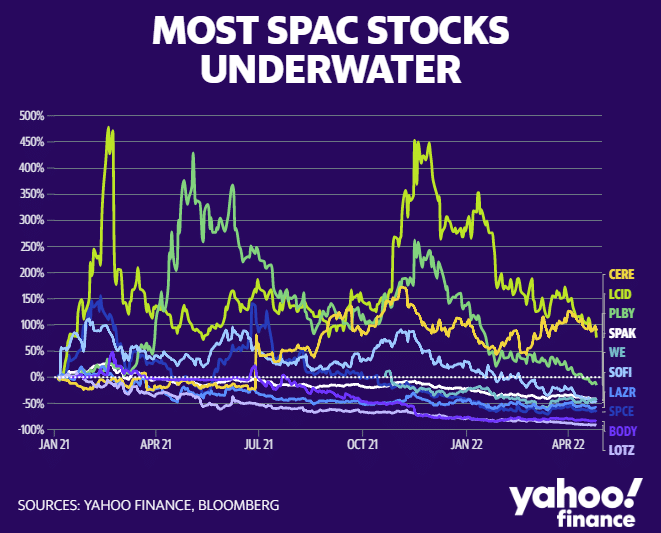

There are still over 950 SPACs seeking to raise $239 billion from investors. Of this, $207 billion worth haven’t even found a target. Since the beginning of 2021, most of these SPACs are now underwater.

In hindsight, we now know that only Wall Street benefited by dumping a supply of speculative products to retail investors armed with a stimulus check and a trading app. Wall Street reaped the rewards of bringing these companies public and selling their shares at premium values to unsophisticated investors under the well-crafted story of “innovation.”

Not surprisingly, retail investors lost. Wall Street wins.

But, as shown, by the end of 2021, most IPOs and SPACs failed to work as well as hoped.

Lessons Learned And Relearned

The amount of speculation in the market in 2020 and 2021 was a warning sign that was easy to see. Yet, no one did. However, such is always the case when investors allow greed to trump basic logic.

As we noted then:

“The three most significant market risks heading into 2022 are a reversal of the things that supported the speculative attitude of investors over the last year: buybacks, liquidity, and earnings growth. Notably, the reversal of liquidity impacts every facet of the economy and markets, and earnings are the “bullish support” for overvaluation.”

Such was the case in 2022, which had the worst start to any trading year since the Great Depression.

As is always the case, investors must often relearn lessons the hard way during market cycles. Long bullish advances desensitize investors to the risk they are taking. Investors can take on leverage or buy poor fundamentals, and rising prices will cover those mistakes.

Unfortunately, when the “tide eventually goes out,” those mistakes are revealed in the most brutal of fashions.

Conclusion

Such is why, as an investor, the most important investing attribute is to step away from your “emotions” and look objectively at the market around you. As Howard Marks once quipped:

“In good times skepticism means recognizing the things that are too good to be true; that’s something everyone knows. But in bad times, it requires sensing when things are too bad to be true.

The things that terrify other people will probably terrify you too, but to be successful an investor has to be stalwart.

After all, most of the time the world doesn’t end, and if you invest when everyone else thinks it will, you’re apt to get some bargains.“

How you choose to manage your portfolio is entirely up to you. Every investment strategy has a consequence and will lose money from time to time.

The only difference is the amount of the loss, what causes it, and what you do about it.

The post Wall Street Wins Again – SPAC Edition appeared first on RIA.