{kind=link}

This past winter included some tumultuous weather events with implications for global energy markets. Winter storm Uri exposed vulnerabilities in the Texas power grid, and left millions without heat during an unusually cold snap (see Why Texas Lost Power). All power sources provided less than needed – some blamed the state’s excessive reliance on windmills, many of which iced up rendering them unusable. Others note that natural gas also came up short, although it was the only energy source able to increase its output.

Texas has its own power grid (overseen by the Electricity Reliability Council Of Texas, or ERCOT) which is lightly regulated. Electricity is cheap, but providers aren’t required to guarantee 100% continuous supply. The February price spike in natural gas created a windfall gain for some pipeline companies including Energy Transfer and Kinder Morgan (see Why The Energy Transition Is Hard). It was the only source of energy able to respond to price signals.

Renewables are intermittent, working best when it’s sunny and windy. Bad weather can take all solar and wind offline simultaneously. For grid managers this is analogous to owning a portfolio of investments that provide diversification except during a big market fall, when it’s most needed. Solar panels and windmills generate power only 20-30% of the time, operating at far lower capacity than combined-cycle natural gas power plants. Reliable power means natural gas.

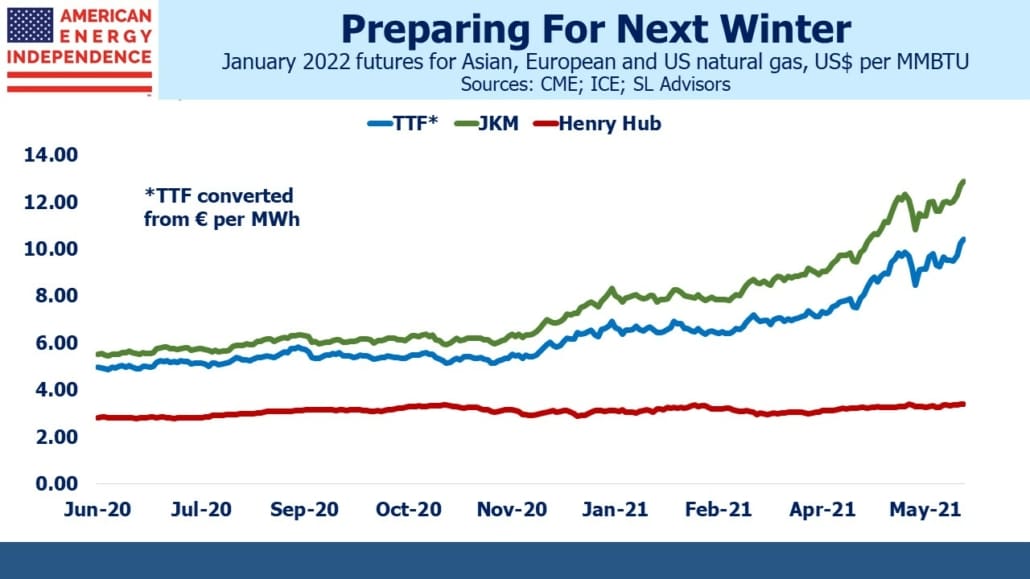

North east Asia also endured a surprising cold spell in January. The JKM benchmark price for Liquified Natural Gas (LNG) exceeded $20 per Million British Thermal Units (MMBTUs). US natural gas prices are remarkably stable, generally not moving too far from $3 per MMBTU.

The Asian spot LNG price rose 10% last week to $12 per MMBTU amid continued robust demand. Looking ahead to prices for January 2022, both the JKM Asian benchmark and the European TTF futures have been rising in recent months, widening the spread with the US Henry Hub benchmark. The price difference is comfortably enough to cover liquefaction, transportation and regasification of US natural gas to markets in Asia and Europe. American energy will be helping keep Asians warm this winter.

As a result, American exports of reliably cheap LNG are drawing the attention of global buyers. Tellurian (TELL) is a recent beneficiary, having signed ten-year agreements with Gunvor and Vitol to provide each with 3 million tons per annum of LNG (see Profiting From The Efforts Of Climate Extremists). These commitments have improved the odds that Tellurian will be able to finance and build the Driftwood LNG export facility in Texas.

Green energy policies are helping – TELL CEO Charif Souki has noted that European carbon taxes act as a floor on local natural gas prices by penalizing coal. TELL’s previous strategy was to sell natural gas to buyers at a price linked to the US benchmark, but foreign buyers prefer to lock in prices against their local benchmark. TELL’s recent deals have retained this spread risk for the company,

The market is taking advantage of cheap US natural gas. This helps lower emissions, both by reducing coal consumption but in some cases by providing reliable back-up for increased use of renewables. If the logic of this strategy penetrates the thinking in the Biden administration, they may start advocating for increased exports of US LNG, which could raise domestic prices.

However, building LNG export capacity is costly and time-consuming. Environmental extremists in Oregon have thrown up enough roadblocks to Pembina’s planned construction of the Jordan Cove LNG export facility that it’s unlikely to be completed. So while the arbitrage spread between US and foreign natural gas markets ought to close, physical constraints on US exports may allow it to persist for several years.

On a different note, the International Energy Agency (IEA) drew headlines last month when they published Net Zero by 2050. Director Fatih Birol said, “The pathway to net zero is narrow but still achievable. If we want to reach net zero by 2050 we do not need any more investments in new oil, gas and coal projects.” Driving up fossil fuel prices by constraining supply is a logical way to increase renewables demand, by improved relative pricing.

Last week the IEA showed how confused they are by saying that, “OPEC+ needs to open the taps to keep the world oil markets adequately supplied.” This is their recommended response to rebounding oil demand. That they are advocating for reduced long term supply but more short-term supply betrays an incoherent thought process not worth the attention they get. St. Augustine’s spirit, (“give me chastity, just not yet”) often resolves the internal conflict in switching from today’s efficient energy sources to intermittent, less efficient “green” alternatives. A more thoughtful IEA would advocate for more natural gas supply over all time frames, to reduce coal consumption and support electrification. They’re just not there yet.

We are invested in all the components of the American Energy Independence Index via the ETF that seeks to track its performance.

The post Global Natural Gas Demand Is Rising appeared first on SL-Advisors.